Want help to write your Essay or Assignments? Click here

Evaluating Returns and Cash Flow Streams

Overview

Solve nine problems addressing a range of issues related to valuation of stocks, bonds, annuities, and cash flow streams.

The result of a financial manager’s efforts is ultimately reflected in stock price; maximizing shareowner wealth is what finance is all about. This assessment examines the classic financial tradeoff of risk versus reward.

By successfully completing this assessment, you will demonstrate your proficiency in the following course competencies and assessment criteria:

- Competency 1. Maximize shareholder wealth.

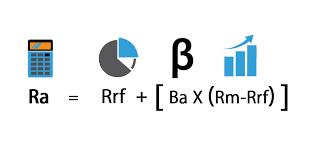

- Calculate the required return on a portfolio fund.

- Calculate the required rate of return.

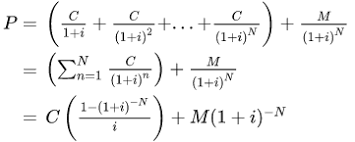

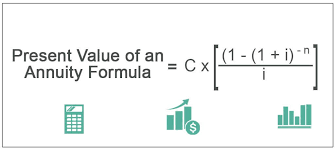

- Compute the present values of ordinary annuities.

- Competency 3. Evaluate capital expenditure investment projects.

- Calculate bond evaluation.

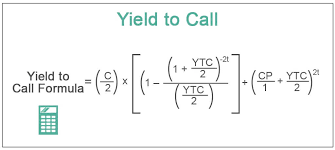

- Apply computations to explain yield to call.

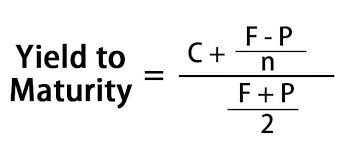

- Calculate yield to maturity using correct calculations.

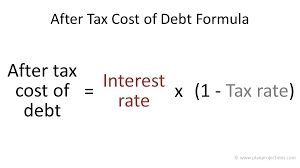

- Compute the after tax cost of debt.

- Competency 5. Apply evaluation principles of various financial instruments.

- Explain uneven cash flow streams.

Evaluating Returns and Cash Flow Streams

Want help to write your Essay or Assignments? Click here

Context

Stocks

Maximizing shareowner wealth is all about increasing the stock price. Risky investments require higher returns, so when financial managers take greater risks, the logical reaction of shareowners is to demand a higher return. How do they accomplish this? If you were a bondholder, you would require a higher interest payment, but as a shareowner, you get higher returns by lowering the stock price.

So it may appear that a business should be averse to risk because it runs counter to the notion of a higher stock price, but in fact, businesses must take risks to get those higher returns. When relatively risky ventures pay off, or when shareowners believe management can pull it off, the stock price can soar.

Bonds

It is important to examine the main categories of bonds, long-term instruments such as Treasury bonds, corporate bonds, municipal bonds, and foreign bonds. All bonds share certain common features such as face or par value, coupon rate, maturity date, and other provisions. Some bonds are sold at a deep discount and do not provide any coupon interest payments; these are called zero-coupon bonds.

Previously we have talked about the fact that the value of any financial asset should be based on the present value of its future cash flows. This holds true for the valuation of bonds as well. There are different numerical tools used in assessing and comparing different bonds such as yield-to-maturity, current yield, and yield-to-call for callable bonds.

Our analysis of bonds would certainly be incomplete if we did not consider the risks involved in purchasing different types of bonds. Interest rate, reinvestment rate, and default risks are all associated with the investment in bonds. One important observation regarding the bond markets is that they rely on several independent bond rating agencies providing continuous monitoring of the most important bond issuers.

Evaluating Returns and Cash Flow Streams

Want help to write your Essay or Assignments? Click here

Cash Flow

An asset’s value depends on the valuation of the after-tax cash flows this asset is expected to produce.

Questions to consider

To deepen your understanding, you are encouraged to consider the questions below and discuss them with a fellow learner, a work associate, an interested friend, or a member of the business community.

- Analyze some of the most important elements of the current tax laws, such as the differences between the treatment of dividends and interest paid and interest and dividend income received. How can financial managers increase shareholder value through managing tax obligations?

- Examine the company you work for (if your company is not publicly held, pick a company you are familiar with), and consider the following.

- Would you consider this company to be relatively risky? Does the stock rise and fall faster than the market?

- What things contribute to the riskiness or stability of the stock?

- What is the CAPM and security market line, and how can they be used in assessing share price?

- The time value of money is defined as the math of finance for which interest is earned over time by saving or investing money. Why does time value affect almost any financial decision? Under what situations might time value matter less?

- Examine the importance of bond ratings and some of the criteria used to rate bonds. Differentiate between interest rate risk, reinvestment rate risk, and default risk. How would a financial manager use bond ratings to increase the value of the firm?

- Examine what is meant by the statement that a preferred stock is a hybrid between a common stock and a bond. What factors determine the value of a share of preferred stock?

- Identify some of the factors that would cause you to rely more on either NPV or IRR. Does MIRR solve all of IRR’s shortcomings?

Evaluating Returns and Cash Flow Streams

Want help to write your Essay or Assignments? Click here

Resources

The following optional resources are provided to support you in completing the assessment or to provide a helpful context. For additional resources, refer to the Research Resources and Supplemental Resources in the left navigation menu of your courseroom.

- Konchitchki, Y. (2011). Inflation and nominal financial reporting: Implications for performance and stock prices. The Accounting Review, 86(3), 1045–1085.

- Jiraporn, P., Kim, J., & Kim, Y. S. (2011). Dividend payouts and corporate governance quality: An empirical investigation. Financial Review, 46(2), 251–279.

- Pratt, S. P., & Grabowski, R. J. (2010). Cost of capital: Applications and examples (4th ed.). Hoboken, NJ: John Wiley & Sons.

- Chapter 8: Capital Asset Pricing Model.

- Chapter 10: Beta: Differing Definitions and Estimates.

- Sherman, E. H. (2011). Finance and accounting for nonfinancial managers (3rd ed.). New York, NY: Amacom.

- Chapter 6: Relating Risk and Return, Valuation, and Time Value of Money.

- Parameswaran, S. (2011). Fundamentals of financial instruments: Stocks, bonds, foreign exchange, and derivatives. Hoboken, NJ: John Wiley & Sons.

- Chapter 4: Bonds.

- Downes, J., & Goodman, J. E. (2014). Dictionary of finance and investment terms (9th ed.). Hauppague, NY: Barron’s.

- Brigham, E. F., & Houston, J. F. (2016). Fundamentals of financial management (14th ed.). Boston, MA: Cengage.

Want help to write your Essay or Assignments? Click here

Assessment instructions

For this assessment, complete Problems 1–9 to apply the necessary knowledge to assess returns and cash flow streams. You may solve the problems algebraically, or you may use a financial calculator or an Excel spreadsheet. In addition to your solution to each computational problem, you must show the supporting work leading to your solution to receive credit for your answer. Note the following:

- You may need an HP 10B II business calculator.

- You may use Word or Excel, but you will find Excel to be most helpful for creating spreadsheets.

- If you choose to solve the problems algebraically, be sure to show your computations.

- If you use a financial calculator, show your input values.

- If you use an Excel spreadsheet, show your input values and formulas.

Want help to write your Essay or Assignments? Click here