Want help to write your Essay or Assignments? Click here

The Impact of Brexit on the UK and the EU’s financial regulation

Introduction

The 1999 EU regulatory initiatives were meant to ensure that there were maximum financial markets activities among member countries. The regulations were also meant to contribute to the removal of existing legal barriers in the financial sector among EU members. The cross-border financial market initiative benefitted the UK and contributed to an increase in trade in the sector. However, Brexit’s move on 23rd June 2016 might have resulted in an end to the many of the financial conveniences that the UK enjoyed (Grant Thorton, 2016).

According to Wellink (2009: 13), and World Bank (2013: 15), regulatory arbitrage is one of the greatest disadvantages that can emerge from an exit of a country from a Union with existing guidelines and policies. According to Wen (2016), there is a possibility of businesses undercutting each other if the current financial market is deregulated. Brexit might contribute to deregulation of the UK’s financial sector, therefore contributing to undercutting of some firms through unscrupulous dealers. Some of the firms that have their headquarters in the region might initiate planning on moving to other regions that they consider favourable; especially those within the European Union coverage.

Institutions in the global financial market will be affected to great lengths as a result of Brexit. Institutions that are directly related to the UK or the European Union might have to “revise” the location of their headquarters or location of their subsidiaries. The adjustments are necessary for the firms to survive in the market. Brexit has a major impact on financial firms because the sector is strictly regulated, and might contribute to challenges especially for UK firms.

Impact and challenge of Brexit on the UK’s financial sector regulation

According to Claessens and Kodres (2014: 78), regulation of the financial sector contributes to securing of firms so that the shareholders’ wealth is maximized. The UK financial institutions will have to meet the requirements of strict regulations which emanate from Brussels. Before Brexit, the UK might have had an upper hand in negotiating for strict financial regulations such as their refusal on the imposition of tax bonuses. However, the EU might want to use them (UK) as an example of the disadvantages that countries are bound to face when they exist the EU.

The regulatory arbitrage for the UK might have complex consequences since some of the financial sector regulations for the UK and EU are different. The UK might have more strict rules in comparison to those that are issued by the EU. The EU might have less stringent rules based on the need to accommodate many different members who have different backgrounds.

The UK has been part of the EU for over forty years, and most of its financial sector laws are based on policies in the EU regulations. Therefore, Brexit could contribute to instability of the UK banking system since most of the financial regulations that have been in use, have not been enshrined in the UK law for the forty years that the country has been a member of the EU. The effects from pass porting will determine the future of the financial sector for the UK. It is not all gloom for the UK’s financial sector after Brexit since the country will attain independence to make its own decisions in the sector.

Any loopholes that might be used by firms for arbitrage purposes should be identified and sealed so as to minimize any chances of illegal activities. Banker bonus cap has been raised as one of the areas that the bank of England and the European Parliament discussed as possibly contributing to financial regulation arbitrage.

There will be immediate need of business continuous amidst the new and old regulations, or lack of clarity in the regulations that should be applied. Existing international financial firms that are located in the UK will have to make decisions on the viability of their current location. If the firms decide on a new location within the EU, they will have to make assessments on the suitability of a location that will contribute to a high level of business.

The short duration of confusion might lead to loss of business for some international firms. Financial firms in the UK will also have to ensure that they follow the MIFD II rules that will be established in 2018. The UK’s economy will be negatively impacted by a move of the financial firms that will want to relocate especially from London. Most of the international firms owned by EU member countries might want to relocate to other capital cities within the EU in order to make maximum gains.

The UK owned financial firms that have been conducting business in the EU will face higher costs and double rules if they will continue trading within the EU (Ashurst, 2016: 4). The low costs and EU financial regulation rules will no longer be accessible to those firms. Companies in the UK will also face stringent measures as required by the European Commission and the UK in the acquisition of partners from the EU.

The regulatory authorities in the UK are likely to increase the sector’s interest rates so as to make up on the deficit from being charged high rates through trade involving the EU. Clients will consider financial firms in the UK as being less stable as compared to those in the EU. Therefore, the clients might ask for higher returns on their investment based on the higher level of risk.

Financial firms will in turn have to invest in projects that have a high return, but take a long duration to give the expected profit on the investment made. The regulation of the financial sector institutions and supervision is largely national, even if the country is a member of a larger body (Omarova, 2010: 665: International Monetary Fund, 2009).

Evaluation of UK and EU’s financial regulation

The EU is quite strict on “bailing out” of companies since it results in the depression of the economy. Funds that could have been injected into projects contributing to the development of the economy, or boosting the economy are put into several companies that might not have a major positive impact on the economy (Heath, 2013: 32). Bailing out of companies by the government might contribute to lowering of ethical standards in companies.

The companies would know that the government would bail them out in the event that they collapsed. UK based financial companies are bound to face strict regulation especially since clients are likely to demand higher returns based on the higher level of risk. The EU is viewed as contributing to stability among its member states, and therefore making transactions that they engage in safer and more likely to give the planned return.

Want help to write your Essay or Assignments? Click here

The consequence arbitrage that has resulted from Brexit is highly influenced by non-financial effects of the initiative. The UK is no longer being considered as a major stakeholder in the making of foreign policies that might be required in times of conflict. Therefore, the UK has less bargaining power if it requires making deals with other countries. It is critical for a country to have a high bargaining power so as to negotiate trade and profitable financial agreements for its institutions (Weil, Fung, Graham, and Fagotta, 2006: 68).

The consequence arbitrage is the exit of major international financial institutions from London to other European Union capital centres. International financial organizations such as banks have already operated in the European Union and in the EU for decades. The move will contribute to the undoing of many years work, since the UK government has made numerous deals to bring the firms into the country (Ashurst, 2016: 4). Governments usually have to spend reasonable resources and adjust their regulations so as to be attractive to investors from foreign organizations.

Many other countries usually compete for the foreign firms. Therefore, countries have to ensure that their package offers are as friendly as possible. Furthermore, a financial Maginot line is necessary to deal with any eventualities that might arise such as collapsing of hedge funds. A hedge fund with a large volume of deposits could collapse and contribute to the collapse of banks in the region. The collapse or discovery of missing funds in a hedge fund could be triggered by sudden national financial moves such as the one triggered by Brexit.

Clearing houses might also contribute to negative consequences in the financial sector. According to Wen (2016: 9), clearing houses deals defaulting by a few traders can contribute to the system’s collapse. The collapse would result from the system’s insolvency. The central banks in different nations oversee the financial systems of those countries. However, there is no institution to oversee the central banks of different countries.

In the event of a collapse of the central banks of the countries involved in Brexit, there would be a collapse of all other financial institutions in involved nations. Financial regulatory organizations are focused on maintaining the regulations in place, especially because of the hefty fines that have been put in place. Therefore, in the event that the central bank was collapsing, it might take time for signs to be recognized by the financial firms that are the major focus of regulation.

Want help to write your Essay or Assignments? Click here

4.0 Conclusion

If it would not make the UK appear inconsistent, I would recommend a return to the European Union. However, since the decision and necessary steps have already been taken, the UK has to make do with its current situation. The UK has to establish clear guidelines in its financial sector since it has mostly used those in the European Union for about forty years. The opportunity should be utilized in coming up with financial sector regulations that will promote growth and have a competitive edge over countries in the European Union.

The regulatory authorities in the UK are likely to increase the sector’s interest rates so as to make up on the deficit from being charged high rates through trade involving the EU. However, the UK will have to come up with clear financial policies so as to mitigate the occurrence of a crisis. In the past, there has been severe and a high level of frequency of financial crisis that have occurred across the globe. The regulation and supervising of firms in the financial sector of a country is largely a national responsibility.

Both regulation and consequence arbitrage results are likely to be experienced by countries in the UK due to its exit from the European Union. There are international banks that have been situated in the UK for a long duration. These firms might have to relocate to other geographical locations in the EU so that they can continue enjoying the same regulations that they are used, especially if their parent firms are located in Europe (Ashurst, 2016: 6).

The geographical move would result in loss of revenue and employment for many UK nationals. Financial firms in the UK would be motivated to move because they would be expected to comply with a double regulation of the financial sector in EU, and that of the UK. Clearing houses could also contribute to a major collapse of the financial sector as a consequence of a failure of payment by a few dealers especially if they trade in high volumes. The solution to the possible loopholes that might occur is strict regulation of the financial sector for both the UK and EU.

Bibliography

Ashurst, 2016, Brexit: potential impact on the UK’s banking industry. Ashurst.

Claessens, S. and Kodres, L. 2014, The Regulatory Responses to the Global Financial Crisis: Some Uncomfortable Questions, IMF Working paper.

Heath, R., 2013, “Why Are the G-20 Data Gaps Initiative and the SDDS Plus Relevant for Financial Stability Analysis?” IMF Working Paper 13/6 (Washington: International Monetary Fund).

International Monetary Fund, 2009, “Restarting Securitization Markets: Policy Proposals and Pitfalls,” Chapter 2 in the Global Financial Stability Report (Washington: International Monetary Fund).

Omarova, Saule T., 2010, “Rethinking the Future of Self-Regulation in the Financial Industry,” Brooklyn Journal of International Law, 35, (3): 665.

Weil, D., Fung, A., Graham, M., and Fagotta, E. 2006, “The Effectiveness of Regulatory Disclosure Policies,” Journal of Policy Analysis and Management, Vol. 25, No. 1, pp. 155-81.

Want help to write your Essay or Assignments? Click here

Fermi Problems

Fermi problems are an estimated problem that is used to dimensional analysis and approximation and is often a back-of-the-envelope calculation. This type of estimation technique was named after the physicist Enrico Fermi, who was widely known for his approximation calculation prowess and at times, with little or no data. Fermi problems are used to justify guesses about their quantities and variance. Enrico has received worldwide recognition for most of his accomplishments, but the major one is his contribution to the development of the atomic bomb.

The talk by Lawrence is significant for physicians primarily to understand Fermi problems. Lawrence gives his viewers a physicist’s perspective of the world. He does so with the help of experiments, for example, he drops a book and a paper and asks which fall first while giving the explanation why the book fell first.

Want help to write your Essay or Assignments? Click here

The first of Fermi problems revolves around counting the number of equipment that is in a particular region for example piano tuners (Krauss, 2008). The first question is the number of people in the population, how many use keyboards and the number of families that own pianos. The second issue revolves around the number of substances that can fill another subject, for instance, the number of water balloons that can fill a room. One thing is to note the quantity of water that a single balloon can hold and the amount of water required to fill the room. Form there a simple calculation is exerted to find the number of approximated balloons and water.

There is a good chance that every time an individual breathes he/she takes in one molecule that was inhaled by Julius Caesar before his assassination. This was achieved using Avogadro’s number (6.02×10²³) and which multiplies the number of molecules in a single breathe and the atmosphere. The next step is finding out the volume of the atmosphere and through calculation arrives at the number of molecules that are consumed by each person.

The number of piano tuners in London varies from 50 to 125. This can be arrived by viewing the whole population in London and estimating the number of households that own one and calculating the number of houses that regularly tune a piano and how many times a piano can tune in a day.

Reference

Krauss, L. (2008). Commentary: World Lines by Lawrence Krauss. New Scientist, 198(2653), 50.

Want help to write your Essay or Assignments? Click here

According to economists, there are different ways of measuring the growth of an economy. According to Baldwin and Borrelli (2008), Gross Domestic Product is the commonly used measurement tool used to measure the economic growth of a given country. Nevertheless, certain economists believe that GDP is not a fully reliable method of measuring the growth of an economy.

In certain countries and institutions, improvement of the living standards can also be used as a tool for measuring the economic growth (David, 2005). GDP and other metrics such as unemployment rates, living standards, and inflation rates can help in determining the actual economic growth. Additionally, factors such as spending versus productivity can also help in quantifying the level of economic growth.

Comparative advantage and Absolute Advantage

According to David (2005), absolute advantage is the difference in the productivity of various countries while the comparative advantage denotes the differences that are there in the opportunity cost. Ideally, using smaller inputs to produce a large quantity of produce is known as an absolute advantage while the ability to produce at lower opportunity cost is a comparative advantage.

Therefore, certain countries such as China and the US have the absolute and comparative advantage at some point (Baldwin & Borrelli, 2008). For instance, the US use fewer resources to produce a given product compared to other countries. However, countries like China have a comparative advantage when they produce specific products at relatively lower margins.

Both absolute and comparative advantage are two main important factors for the international trade. These factors elaborate how different nations use the little resources that they have to produce given quantities of produce (Hansen, 2012). However, the advantage and the disadvantage of a country also depends on its choice of goods to produce.

For other countries, devoting resources and manpower to other countries limits competition. For example, the US would devote resources to the vehicle-producing Japan rather than compete with it. In which case, Japan would have the absolute advantage while the US has a comparative advantage.

China

Studies have revealed that China is one of the countries that continue to enjoy the advantage of its resources and human resources (Seretis & Tsaliki, 2016). China has overtaken countries like Japan to become the second-largest manufacturer after the US. Ideally, the country enjoys low labor costs while producing most of its products (David, 2005).

For China, the human resource is still an absolute advantage over many nations. The vast labor supply attracts larger investments and companies in the region. Compared to places such as the US where the human resource is declining, China enjoys a bigger absolute advantage (McConnell, 1999).

GDP Growth Rate in China

The Chinese economy has grown to 6.7% in 2016, which is by the expectations. The GDP growth in China has been successful hitting a high rate at 15.4% in 1993.

USA

Unlike China whose production is labour-intensive, the US enjoys a comparative advantage by using its specialized labor resource. In as much as the labor resource in the US is abundant, the country’s main advantage is that its human resource is skilled. As such, the US can produce high-quality products using its rich and skilled human resource.

GDP Growth in the US

The GDP in the US increased to 2.9% in the third quarter of 2016 1.4% higher than the last quarter. However, the increase is attributable to personal expenditure increases, the increase in exports, inventory investments as well as the increased federal government spending.

Saudi Arabia

Unlike other countries such as China and the US, Saudi Arabia is a country that relies on a single vast natural resource. According to Hansen (2012), this country would be poor without the large oil reserve. However, the nation enjoys a natural comparative advantage over other countries. With its large oil reserve, the country can engage in a profitable international trade with other major countries. As such, Saudi Arabia continues to enjoy a wealth of natural resource that gives it the extreme comparative advantage.

GDP growth Saudi Arabia

Saudi Arabia GDP grows at a rate of 0.5%. The Trading Economics analysts, the rate will remain 0.5% at the end of this quarter. However, the long-term growth rate is projected to increase to 3.5%.

Democratic Republic of Congo (DRC)

Likewise, DRC is another country that enjoys the vast amount of natural resources. This country has large scale diamonds and copper compared to other countries. With its large scale natural resources, this country enjoys an absolute advantage when it comes to trade. The GDP of DRC increased from $241.87 to $306.1 between 2009 and 2016. This, therefore, makes 2% of the global GDP.

Annual GDP Growth Rate

Unlike the increased GDP growth rates in most countries with absolute and comparative advantages, DRC remains one of the countries whose GDP is sluggish. The outraging political conflicts in DRC makes it hard for them to enjoy a stable economy. The growth rate in 2016 remains at 4.6%, which is low by 0.2% from the last rate.

Variance in Economies

The GDP growth varies across countries of various continents. However, Ural (2007) maintains that there are four main factors that determine the variations. The main factors that lead to variations in the GDP growth across countries include differences in the workforce, physical capital, human capital and technology differences (Shelburne, 2016).

Workforce Differences across Countries

The differences in workforce across countries affects the rate of GDP growth and the growth of the entire economy. Ideally, the differences depict the amount of labor that a given country has towards its production (Rnskov & Foss 2016). Countries like China have vast workforce I term of human resource. This helps them during production because they can get abundant labor as compared to other countries such as Saudi Arabia.

On the other side, the level of the workforce can also help a country in ensuring a large scale production. The abundant labor force is advantageous in production. As such, nations such as the US, China and India tend to have higher economic growth than the other countries.

Difference in Physical Capital across Countries

Physical capital is a determinant of economic growth. The larger the physical capital of a country, the stronger the economy of that country. For example, the US has a capital stock of $30 trillion compared to smaller countries such as DRC and Saudi Arabia. Although China’s physical capital is also high, analysts believe that the US enjoys more efficiency in production due to a larger physical capital that the nation has (Hansen, 2012). Physical capital helps a country to fund its production efficiently without outsourcing for credits. This makes various nations different from one another.

Human Capital Differences

Human capital refers to the value of the human resource that a country has. In most cases, developed countries have more valuable human resource than less developed countries. Grandke et al. (2015) reiterated that the value of human capital is measured by determining the level of education and level of skills that individuals of a given country possess. According to McConnell (1999), the level of education is correlated to the GDP growth.

Therefore, the differences in literacy levels in various countries lead to variations in the economic growth of different countries. For example, the US has high literacy levels than DRC and Saudi Arabia. Conversely, this affects the levels of expertise and skills that the human resource has in such countries. This difference explains why China and the US produce larger amounts of products that DRC and Saudi Arabia (Ural, 2007).

Technology Differences

Technology is fundamental in the production and growth of an economy. Rnskov and Foss (2016) opine that despite capital, human resource and workforce levels, the availability of technology also helps in determining the rate of production and consequently the economy. Through Research and Development, large firms can acquire knowledge and skills of producing various products (Shelburne, 2016).

To produce efficiently, individual countries must use the right technology. Nonetheless, the cost of employing the right technology in production can only be met by specific countries that have stronger and stable economies. For example, countries such as China and the US have the capacity to acquire the right technology for production. On the other hand, countries such as DRC lack the adequate capital to acquire the right technologies in production (Seretis & Tsaliki, 2016).

In most cases, countries such as Saudi Arabia and DRC will import technology from other countries such as China and the US. Technology increases efficiency. Thus, it determines the levels of output. The nature of the technology used by a particular company helps in achieving a high level of production (Rnskov & Foss, 2016).

Trade and the Strength of Economy

Trade is one of the drivers of economic growth. International trade is attributable to economic development by reducing the levels of poverty while increasing the commercial opportunities for countries. Through trade, countries like China and Saudi Arabia have expanded their production rates. Additionally, trade increases the value of investments in various countries as they go up into the global value chain.

The international trade facilitates diversification of exports thus, helping countries to access fresh markets internationally. On the other side, trade ignites innovation through the exchange of technologies and expertise (Grandke et al. 2015). It is through trade that countries such as China and the US have the ability to create employment opportunities to their populations. Moreover, trade helps in stabilizing the relationships between various nations thus, creating peace and harmonious environments that facilitate development (Shelburne, 2016).

Lifecycle of Trade

Trade life cycle comprises of the stages that the trade goes through. With the predicted outcomes and objectives at hand, trade life cycle is supposed to represent the forecasted events. Grandke et al. (2015), acknowledge that stages of a trade determine the progression of the trade from its inception throughout its progression. Different countries go through different stages of trade life cycle.

To execute a trade, various processes and procedures must be followed. Ideally, the stages determine the success or failure of the trade. In most cases, the processes start with the execution of trade after the agreements have been made. In cases of international trade, Rnskov and Foss (2016) note that the stages of trade are determined by the progress made in previous stages (Shelburne, 2016). For instance, countries such as China and the US have established trade lifecycles compared to developing countries such as DRC. Based on a country’s resources, trade lifecycle can be efficient.

References

Baldwin, N., & Borrelli, S. A. (2008). Education and economic growth in the United States: Cross-national applications for an intra-national path analysis.Policy Sciences, 41(3), 183-204. doi:http://dx.doi.org/10.1007/s11077-008-9062-2

David, H. L. (2005). So many measures of trade openness and policy: Do any explain economic growth? (Order No. 3179497). Available from ABI/INFORM Collection. (305006923). Retrieved from http://search.proquest.com/docview/305006923?accountid=45049

Grandke, F., Singh, P., Heuven, H. M., De Haan, J. R., & Metzler, D. (2016). Advantages of Continuous Genotype Values over Genotype Classes for Gwas in Higher Polyploids: A Comparative Study in Hexaploid Chrysanthemum. Bmc Genomics, 171-9.

Hansen, T. J. (2012). The use of business tax incentives: An analysis of the economic performance of minnesota’s JOBZ (job opportunity building zones) program (Order No. 3503148). Available from ABI/INFORM Collection. (1009056994). Retrieved from http://search.proquest.com/docview/1009056994?accountid=45049

Mazurek, J. (2015). A Comparison of GDP Growth of European Countries during 2008-2012 from the Regional and Other Perspectives. Comparative Economic Research, 18(3), 5-18.

McConnell, I. E. (1999). Trade and the environment: Defining a role for the world trade organization (Order No. NQ41085). Available from ABI/INFORM Collection. (304561048). Retrieved from http://search.proquest.com/docview/304561048?accountid=45049

Ørnskov, C., & Foss, N. J. (2016). Institutions, Entrepreneurship, And Economic Growth: What Do We Know And What Do We Still Need To Know? Academy Of Management Perspectives, 30(3), 292-315.

Rnskov, C., & Foss, N. J. (2016). Institutions, Entrepreneurship, And Economic Growth: What Do We Know And What Do We Still Need To Know? Academy Of Management Perspectives, 30(3), 292-315. Doi:10.5465/Amp.2015.0135

Seretis, S. A., & Tsaliki, P. V. (2016). Absolute Advantage and International Trade. Review of Radical Political Economics, 48(3), 438-451

Shelburne, C. R. (2016). Long-Run Economic Growth: Stagnations, Explosions and the Middle Income Trap. Global Economy Journal, 16(3), 433-458.

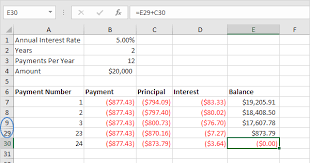

An amortization schedule refers to a tabular presentation of the mortgage loan payment schedule, indicating the interest and principal amount paid until the loan is repaid fully (Brechner & Bergeman, 2014). An amortization calculator is used in developing the schedule, based on the amount, interest rate and repayment period. The amortization schedule is generally utilized for identifying the amount paid, to both interest and principal, and the outstanding balance.

An amortization schedule helps in the generation of identical payment over the repayment period, such that the entire amount is paid by the end of the period (Biafore, 2013).

The schedule is used in determining the percentage of interest to be paid during each period in comparison to the principal amount to be repaid. In essence, it separates the portion of payment that covers the interest expense from the portion the premium paid to the principal in each period. Biafore (2013) notes that even though a similar amount of premium is paid towards the mortgage each period, the amount allocated to the principal and interest varies each time.

This variation can be observed from the amortization table. The amortization schedule ensures that the borrower and lender are on the same page with regards to the amount repaid and amount owed. This means that in case of any dispute, the schedule acts as reference on the history of payment and pending balances.

The amortization table is useful to the borrowers in that it is a basis for organizing their finances. The borrower is able to track payments made, interest paid and money owed at any given time; such that they can determine their home equity at any given time. Lenders on the other hand can track what is owed by borrowers.

Response 3

In amortizing the mortgage, a significant amount of the payments paid during the initial months mostly comprises of interest, while the remaining amount is paid to the principal (Biafore, 2013). The payments to interest then start declining as the mortgage is repaid, such that the interest paid in the later years is minimal or none.

Accordingly, the tax deducted based on home mortgage interest is likely to be higher during the initial years when a larger amount of interest is being paid, compared to later years when the interest being paid has reduced significantly. In this regard, it is logical to state that interest paid in earlier years plays a more helpful role in in tax reduction than interest paid in forthcoming years.

Response 4

An ordinary annuity differs from annuity due, mainly based on the timing. While the amount due in ordinary annuity is paid at each period end, an annuity due consists of cash flow series that occurs at each period’s beginning. The second difference is related with payment. In ordinary annuity, the payment done is associated with the period that precedes its date (Ehrhardt & Brigham, 2016).

Examples include mortgage payment, loans and coupon bearing bonds. Payment in an annuity due on the other hand, is associated with the period that follows its date. Examples include insurance premiums and rental lease payments.

Problems

If interest rates are 8 percent, what is the future value of a $400 annuity payment over six years? Unless otherwise directed, assume annual compounding periods.

Future Value (FV) = P x [((1 + r) n – 1) / r]

Where P = Annual payments

r = Interest rate

n = Number of years

FV = 400 x [((1 + 0.08)6 -1)/ 0.08]

= $2,934.37

Recalculate the future value at 6 percent interest and 9 percent interest.

6% Interest

FV = 400 x [((1 + 0.06)6 -1)/ 0.06]

= $2,790.13

9% interest

FV = 400 x [((1 + 0.09)6 -1)/ 0.09]

= $3,009.33

If interest rates are 5 percent, what is the present value of a $900 annuity payment over three years? Unless otherwise directed, assume annual compounding periods.

Present Value (PV) = P [(1 – (1 / (1 + r)n)) / r]

Where P = Annual payments

r = Interest rate

n = Number of years

PV = $900 [(1 – (1/(1+0.05)3))/0.05]

= $2,450.92

Recalculate the present value at 10 percent interest and 13 percent interest.

10 Percent

PV = $900 [(1 – (1/(1+0.1)3))/0.1]

= $2,238.17

13 Percent

PV = $900 [(1 – (1/(1+0.13)3))/0.13]

= $2,125.04

What is the present value of a series of $1150 payments made every year for 14 years when the discount rate is 9 percent?

Present Value (PV) = P [(1 – (1 / (1 + r)n)) / r]

Where P = Annual payments

r = Interest rate

n = Number of years

PV = $1150 [(1 – (1/(1+0.09)14))/0.09]

= $ 8,954.07

Recalculate the present value using discount rate of 11 percent and 12 percent.

11 Percent

PV = $1150 [(1 – (1/(1+0.11)14))/ 0.11]

= $8029.15

12 Percent

PV = $1150 [(1 – (1/(1+0.12)14))/ 0.12]

= $7,622.39

References

Biafore, B. (2013). QuickBooks 2014: The Missing Manual: The Official Intuit Guide toQuickBooks 2014. Sebastopol, CA: O’Reilly Media, Inc.

Health care is a necessity for everyone and the expenses are inevitable. Everyone deserves the health care they need from the right provider at the right time (Quincy, 2016). Another difference is the cost of drugs compared to other nations and a lot of people consider it to be unreasonable. In majority of the countries, there is negotiation done by the government to control drug prices with the manufacturers, but the existence of Medicare Part D denies Medicare to negotiate prices. This is why a branded drug costs higher when bought in the U.S.A. compared to other countries. However, this is beneficial to the doctors because of the higher earning they get if they do this compared to other countries. Additionally, a lot of drug suppliers charge more in the U.S. for medical equipment.

The top drivers of health care are chosen lifestyle, utilization, price inflation and mandated benefits. The society today is a culture that favors diagnosis and treatment rather than living healthily and preventing disease. It is still a necessity for consumers to have a healthy mindset and practice a better lifestyle for disease prevention. Due to the increase in utilization, there has been a rise in health care costs and the forms are not all the same (Smart Business, 2009). There is a total of 70% health care costs that come from employee behavior linked to cancers, diabetes, cardiovascular disease, and obesity. Moreover, advertising deceives consumers and make them think prescriptions and procedures could cure their conditions. This is why consumers end up getting unnecessary treatment and the rise of new technology is also a factor why health care costs increase.

Supply and demand seems to be an automatic reason why health care costs more in the USA. There are two answers for this because there can be an increase in prices due to demand and the other reason is because of limited supply, prices are higher (Theory and Applications of Microeconomics, 2012). However, price is not the only thing that matters in supply and demand in health care because it is a fundamental commodity that is relevant to a person’s well-being. A lot of people want health improvement and this is why they demand for health care. Although, the health’s relationship to health care is not direct because even if health care impacts health, a lot of other things can be a factor. Health is considered as a good, but other goods are more tangible compared to it due to its characteristics. People cannot pass on or trade their health with others, except for certain diseases.

Quality health care had always been a main focus and the medical professionals attempted to improve their practice and give the best care in the world, but the results are not equal. The number of medical practitioners in an area is linked with the type of health care they can provide. Therefore, if there is a shortage in workforce, the quality of health care in the area with fewer medical practitioners are going to suffer. There is a health care reimbursement model to pay-for-performance that provides incentives or penalties from patient outcomes and frequency of readmission (Anderson DNP, RN, CNE 2014). If the workforce is weak, pay-for-performance will suffer in some areas. This will lead to a higher demand for services, but limits the access of patients to health care.

Technology and computers could increase health costs of today since majority of medical equipment needs digital platforms to function properly that makes medical facilities dependent on software. This increases health care costs so it becomes inaccessible to those who cannot afford it. Furthermore, there are a lot of elements that cause an increase in health care costs. And to an average patient, technology gives them helplessness and vulnerability.

One example is echocardiography which has the immense capability to detect ailments and it is safe for everyone. In order to interpret the images, an expert is called to do this. Unfortunately, not all companies have this machine and there is no way to make it inexpensive so any patient can have access to its services (Kumar, 2011). Therefore, technology and computers improve the quality of healthcare, but it contributes to the increase in costs.

Since resources are scarce, organizations have disease management. Those suffering from chronic illnesses need more healthcare attention like hospitalization, physician visits, and prescription drugs. The objective of disease management is to improve the condition of those with chronic illnesses and lessen the use and cost of health care services that are linked to preventing complications (Georgetown University, 2017).

Before the organization implements disease management, they first have to know the population and how patients will enroll. They use demographics to find out which patients are going to need disease management program the most. The chronic diseases such as diabetes, asthma, and hypertension are included.

Furthermore, this increases public awareness which has a significant impact in the way decisions are made on the medical care received by the patient.

1) Rights and advantages belonging to shareholders

Shareholders of a company enjoy following rights and advantages

Ownership right: Shareholders being owners of the company enjoy the right to share residual profits left after paying preference dividend. Their rate of dividend is not fixed. It depends upon the amount of profits. Sometimes they get high dividend in case of high profits.

Control over management: Shareholders can exercise their control over management through the election of their representatives in the board of directors.

The voting right: Shareholders have the right to attend annual general meetings of the company and cast their vote in person or through proxy on various resolutions passed in such meetings. This enables them to participate in corporate and managerial affairs without having to regularly manage affairs directly.

Pre-emptive right: At the time of further issue of shares, an offer is made to shareholders first. If shares are left, they are offered to outsiders. It enables them to maintain their proportionate shareholding intact in the company ( H.Sherman, 2011).

Transfer of the ownership: Shareholders enjoy the right to transfer the ownership of their securities to others by trading their stock on the stock exchange.

2) (a)Differences between the S&P 500 Index and the Dow Jones Industrial Average

Both Dow Jones Industrial Average (DJIA) and the S&P 500 are the best known index of American stocks but differentiate from each other in the following manner.

Criterion

Dow Jones Industrial Average

S&P 500

Introduction

It is an oldest stock market index which was introduced in 1896 by Charles Dow (Johnson, 2015).

S&P 500 was introduced by S&P Global in 1923 and in its current form, it was published in 1957 ( S&P Dow Jones Indices LLC, 2016).

Index Constituents

DJIA is composed of thirty publicly traded American companies listed in NYSE and NASDAQ. These stocks are picked by an editor of The Wall Street Journal. It covers a large range of industries in the US except transport and utilities ( S&P Dow Jones Indices LLC, 2016).

It is based on market capitalization of 500 large companies listed in NYSE and NASDAQ. It covers a wide range of industries.

Weighting Method

It is a price-weighted index which is calculated by taking the aggregate of prices of stocks in an index and divided by a common divisor (Johnson, 2015). The stocks having high prices have more weightage in this index.

It is a free float capitalization weighted index where in components are weighted on the basis of their market capitalization ( S&P Dow Jones Indices LLC, 2016). The stocks with higher market capitalization have more weightage in this index.

(b)Better measure of stock market performance

The S&P 500 is considered to be the better measure of stock market performance than DJIA because it covers approximately 80% of the stock market capitalization and is considered as a true representative of happenings in the US stock market ( S&P Dow Jones Indices LLC, 2016). DJIA covers 30 securities only and its popularity is because of being an oldest index.

3) Differences between common stock and preferred stock

The main two types of stock issued by companies are common stock and preferred stock which have some similarities as well as dissimilarities. The main dissimilarities between both are given as below:

Criterion

Preferred Stock

Common Stock

Meaning

Preferred stock is a hybrid security which combines features of common stocks as well as debt securities (H.Sherman, 2011). The preference dividend is paid at a fixed rate just like payment of interest at fixed rate, but it is paid out of post-tax profits. It is not termed as ownership security.

Common stock is termed as ownership security. Its rate of dividend is not fixed. It depends upon the amount of profits. The amount of dividend may be high in case of high profits and it may be low or even nil in case of low or no profits.

Preferences

Preferred stock carries two preferences over common stock which are (i) Preferred stockholders are paid dividend first before the dividend is declared for common stockholders. (ii) At the time of liquidation of company, preferred stock is redeemed first before any amount is paid to common stockholders (Weaver & Weston, 2001).

Common stock holders are paid their periodic dividend as well as redemption value after satisfying claims of preferred stockholders

Rights

Preferred stocks do not carry any voting right. But holders get entitled to vote when (i) The dividend has remained unpaid for a specified number of years (H.Sherman, 2011). (ii) The resolution to be passed at the meeting has any impact on their interest.

Common stock provides many rights to stock holders which includes voting rights on corporate and managerial issues and preemptive right. Pre-emptive right is the right given to stockholders to maintain their proportionate ownership in the company at the time of further issue of share (Broadridge Advisor Solutions, 2017).

H.Sherman, E. (2011). The Equity in the Business. In E. H.Sherman, Finance and accounting for nonfinancial managers (pp. 204-205). New York: NY: American Management Association.

Weaver, S., & Weston, J. F. (2001). Financial Statements and Cash flows. In S. Weaver, & J. F. Weston, Finance and Accounting for Non-financial Managers (pp. 26-28). New York: NY: Mc Graw Hill.

Want help to write your Essay or Assignments? Click here

Ques1. Explain what a call provision enables bond issuers to do? Why would bond issuers exercise a call provision?

Answer: A call provision is a clause, mentioned in the bond certificate, which enables the bond issuer to repay or redeem bonds before its maturity date at a specified value (Sherman, 2011). Conditions related to time of redemption or buy back of bonds like amount to be repaid and manner in which payment is to be made are mentioned in advance. This call provision is exercised by the bond issuer at the time when the interest rates have fallen and debts are available at cheaper rate in the market. The issuer redeems the bond carrying high rate of interest and issues new bonds with low rate of interest.

Ques.2 Define a discount bond and premium bond. Provide example of each.

The bond issued by the company for the first time is a standard bond. It becomes discount bond or premium bond depending upon the price at which it is being traded in the market.

Discount bond: If the bond is being traded in the market at a price which is less than the face value, it will be termed as discount bond (Weaver & Weston, 2001). A bond becomes discount bond when it gives interest at a rate which is less than the market rate of interest. The investor will be ready to invest in bonds with lower interest rate if the purchase price of such bond is fixed in such a manner that it compensates the investor for less payment of interest in future. For example: A 5% bond is being issued at $1000. The market interest rate is 4%. The investor will be ready to invest in such bonds if the issue price is less than $1000.

Premium bond: If the bond is being traded in the market at a price which is higher than the face value, it will be termed as premium bond. A bond becomes premium bond, it its coupon rate of interest is more than the prevailing interest rate in the market. The issuer will be ready to issue such bonds if the price is fixed in such a manner that it compensates the issuer for higher payment of interest in future. For example: A 5% bond is being issued at $1000. The market interest rate is 6%. The issuer will be ready to issue such bonds if the price is more than $1000.

Ques3. What is the relationship between interest rates and bond prices?

Answer: The fundamental principle of investment in bond market is that there is inverse relationship between interest rates prevailing in the market and bond prices (SEC, 2013).

In market interest rate in bond price

In market interest rate in bond price

If the market interest rate goes up, the investor will be ready to buy bonds with low coupon rate if they are being offered at discount or low price. The investor want compensation for low interest payments to be received in future so he will be ready to buy such debentures if they are being offered at low prices. Similarly if the market interest rate goes down, the investor will be ready to buy the bonds with high coupon rate even at high prices. Thus prices of bond increase.

Ques 4: Describe the difference between coupon bond and zero coupon bond

Answer: The coupon bond is a bond which has coupon rate at which the interest is paid to the bondholder throughout the life of bonds (Sherman, 2011). The bonds are issued with interest coupons and interest is paid to the person who has the possession of coupon. The payment of interest is made at coupon rate and it may be paid quarterly, semi-annually or annually.

Zero coupon bond is a bond which does not carry any coupon of interest as no interest is payable on such bonds. These bonds are issued at deep discount and redeemed at face value on the maturity period. The difference between the issue price and the redemption value is the appreciation value and return for the investor (Weaver & Weston, 2001).

The return for the coupon bondholders is regular in nature whereas the return in case of zero coupon bonds is in the nature of capital appreciation.

Agriculture has been an imperative supporter of the GDP of Bhutan since the absolute starting point. Its commitment to the GDP has been recorded at 38% in the year 1995 with 85% of the populace subordinate upon it; the commitment was 35.9% in the year 2010. In spite of the fact that the commitment of agribusiness declined from 55 % (1985) to 33% (2013) of GDP, despite everything it stays as a prevailing element in the economy of the nation. However, in the most recent decade, the commitment of agribusiness has tumbled to 16.7% of GDP. The issue of accomplishing independence lies intensely on the shoulder of this part as, without improvement of the essential segment, the advancement of the auxiliary area and thusly, advancement of the country can’t be accomplished to the full. The decline of roughly half in 10 years flags that this area requires quick consideration. This examination goes for distinguishing how, the foundation of particular Financial Institutions for Agriculture like; ‘National Bank for Agriculture and Rural Development’ (NABARD, India), can help in building up this segment. This examination endeavors to take shape the part that such particular organizations need to play, since they can give tweaked answers for various necessities in the agrarian segment of a nation, as structures, plans, plans, approaches and methodology, and open the ranchers to the present day innovations and techniques for horticulture.

Introduction

A standout amongst the most imperative parts of the lives of individuals and the financial state of a country is agribusiness. For millenniums, rural exercises have overwhelmed the lives of individuals around the world. In the cutting edge world, horticulture has turned out to be more logical and Innovation situated pointed towards accomplishing higher generation, and in this way, financing farming assumes a crucial part today. This is the place Agricultural Micro finance ends up plainly significant. It assumes an exceedingly critical part in empowering horticultural exercises in many countries. In 2019, there were more than 74 million micro finance borrowers around the world, and the aggregate credit portfolio was about $38 billion USD. On the off chance that we consider Bhutan, horticulture remains the second biggest supporter of GDP quickly after hydro power era. In the meantime, the present rupee emergency in Bhutan has demonstrated that one of the zones in which Bhutan needs to gain a quick and relentless ground is accomplishing self-manageability in nourishment generation. In 2011, Bhutan imported about Nu.286 million worth of vegetables and Nu.1.1 billion worth of rice2, and there couldn’t be a superior time for the country to truly respect the conceivable methods for enhancing its farming generation and diminish its reliance on imports, which channels profitable and hard earned remote cash adding up to Rs.4 billion in the year 2011. The nation has a potential for building up its agribusiness further. One method for achieving this is to guarantee the accessibility of simple credit to the agriculturists in the nation.

This paper endeavors to comprehend the present circumstance of farming micro credit in Bhutan and tries to comprehend the conceivable advantages of extending the extent of rural micro credit and auxiliary administrations through particular foundations in the nation.

Literature Behind Research on Agriculture in Bhutan

On the off chance that we consider micro finance, or all the more particularly microcredit, which concentrates on stretching out little credits to ranchers and was made well known by Grameen Bank in Bangladesh, is a moderately new idea. The advancement and extension of micro finance on the planet can be clarified by the accompanying outline:

2010 – 2012

2012-2014

2014-2015

2015-2017

Expansion

Increase

Commercialization

Transformation

As portrayed by Srnec K., et al. (2018), micro finance establishments around the globe experienced approximately four phases of advancement to be specific, the mid 80’s the place numerous MFIs (micro finance organizations) had a superior rate of return than banks. In the mid 90’s, the place a couple of MFIs started taking care of every one of their costs, a couple of best MFIs started to pull in noteworthy business subsidizing, and were never again restricted to a little gathering of scattered organizations, making it a quickly developing industry and today where MFIs have changed from being casual micro finance foundations to more formal establishments.

The very structure of micro finance foundations has experienced a critical change as of late. Micro finance organizations, as well as standard banks the world over have started to understand the estimation of micro finance and are starting to take into account this division. As indicated by a report distributed by Infosys4, just 28 percent of the aggregate requests for micro finance administrations were secured by the MFIs all inclusive by 2010. The World Bank assessed a micro finance necessity of USD 300 billion out of 2010.

However, in spite of being the centerpiece of provincial and agrarian advancement programs in numerous nations for quite a while, micro finance has likewise pulled in impressive feedback, and many individuals question the adequacy of micro finance establishments. As clarified by Hendrayadi, Irfan, et al, in their paper ‘What is ‘Afflict ing’ the Agricultural Micro Finance Model?’, the objective of the country fund was to advance agrarian improvement through focused medications intended to increment provincial loaning while at the same time decreasing the expenses and dangers to moneylenders. The ultimate result of this approach neglected to achieve its Objective. Initially, sponsored loan costs did not permit provincial back organizations (RFIs) to take care of their expenses. Besides, financed credit extremely regularly focused on the wrong items, which prompted expansion underway wasteful aspects. Therefore, the quantity of nonperforming advances expanded drastically. In the 1970s, horticultural loaning represented more than 30 percent of all World Bank loaning; in any case, by 2010, this number dipped to 10 percent. The measure of Official Development Assistance (ODA) given by OECD nations to rural ventures dropped impressively also. Subsequently, the genuine net guide to farming in the 1990s dropped to a 35 percent of its level in the 1980s.

Another trouble confronted by micro finance establishments around the world was that, in spite of being organizations of simple credit, the loan fees charged by these foundations was still very high. As clarified by Bateman (2011), in the beginning of micro finance organizations, higher rates were important to take care of the high operational expenses of giving small advances to poor people, yet that financing costs would fall in view of rivalry. This contention had some legitimacy at first. In any case, loan costs have not fallen as much as anticipated, and in a few nations (quite Mexico), they have stayed high. To some degree, this was a direct result of the accentuation on.

The business show, with MFIs, now required producing high monetary prizes for their directors (pay rates, rewards) and proprietors/investors (profits and capital increases). Different impediments that hampered the development of micro finance was an absence of legitimate insurance from agriculturists as they were frequently excessively poor, making it impossible to keep resources as guarantee, however as clarified by Llanto (2017), endeavor credits, including advances to poor people (for the most part ladies), did not really require the customary land guarantee as security. MFIs have loaned to resource fewer people and have effectively recuperated the credits. However, nothing from what was just mentioned issues are without arrangement. Bateman (2011) and Llanto (2017) have worried on the requirement for hearty money related control to guarantee that neighborhood budgetary establishments act in a way helpful for maintainable nearby financial improvement and to building and holding neighborhood social capital, yet with a notice that exorbitant direction may suffocate creative micro finance rehearses. Llanto (2017), Hendrayadi, Irfan, et al. what’s more, Miller (2011), have likewise worried on broadening credit portfolios by micro finance foundations, which can be expert by consolidating horticultural advances with different sorts of advances, for example, urban advances, lodging advances, investment funds, protection, etc. Bateman (2011) has even recommended that nearby smaller scale reserve funds ought to be considered as an initial phase in the collection of capital. One of the components unfavourable to establishments occupied with rural loaning as recommended by Llanto (2017) is inordinate government intercession and government endowments, which may not be manageable over the long haul. This is one region where Bhutan ought to be particularly watchful about. We will next consider the micro finance situation in Bhutan and attempt to comprehend its present patterns and future prospects.

Research METHODOLOGY and Design

Planning reasonable strategy and choice of logical instruments is imperative for an important investigation of any exploration issues. This segment is dedicated to the announcement of the technique, which incorporates accumulation of information, examining the system, strategy for investigation and apparatuses of examination.

Gathering of Data

Both essential and optional information has been utilized for the present investigation. An observational study was made among the chosen recipients to get to know the advance sum got, used and reimbursed. On the premise of the data assembled, a very much outlined pre-tried meeting plan was drafted and utilized as a part of the field review to gather the essential information (Vide Appendix-I). Before undertaking the principal review, a provisional meeting plan was arranged and regulated to 25 recipients so as to test the legitimacy of the meeting plan. It encouraged tresearchhe expulsion of the none–response and undesirable inquiries and the altered last timetable in view of this were readied.

The chose recipients were reached face to face and the goals of the examination were obviously disclosed to them and their co-operation was guaranteed. The insights with respect to the general attributes of the example recipients, their families, salary, use, and investment funds identifying with the general targets of the investigation were gathered from the specimen recipients through the immediate individual meeting technique.

Auxiliary wellsprings of information identifying with the readiness to benefit from advances, the number of advances endorsed, advance sums were gathered from the distributed and unpublished reports and records of the BDFCL.

Inspecting Procedure

Bhutan Development Finance Corporation Limited has 22 branches in every one of the twenty locales in Bhutan. With the end goal of gathering essential information from the recipients and recuperation execution, all the 22 branches were incorporated for the present investigation. Out of 22 branches, a sum of 300 borrowers under different plans was chosen indiscriminately for the investigation.

Time Line

Keeping in perspective of the goals of the investigation, 300 example recipients were stratified into two classes specifically, the individuals who have occupied with non-modern exercises and others taking part in mechanical exercises. Out of 300 specimen recipients, 182 (66.67 for each penny) recipients were going to non-mechanical gathering and the staying 118 (39.33 for every penny) fell under the modern gathering.

Objectives of Study:

i. To comprehend the difficulties and openings that specific money related foundations taking into account the farming part have.

ii. To assess the condition of agrarian micro finance in Bhutan.

iii. To propose strategies that may be valuable in assist improvement of such specific monetary establishments.

Research Design: Descriptive research

Information Sources: Optional information gathered from different electronic sources, for example, sites, articles and daily paper diaries accessible on the web, and so forth.

Land reaches out of the examination:

Impediments: The investing+ation is restricted by the way that there has is just a single budgetary organization taking into account rural micro finance in Bhutan. Hence, the measure of data accessible here is very restricted, and not very many examinations have been led identified with this decision, and this has constrained the extent of our investigation.

Research Questions:

Why couldn’t farmers grab the funds in order to approach the require GDP prescribed by the Governmental Agencies of Agricultural Development fields and lands?

What are the major correlations and stats of Agricultural Development Land Authority of Bhutan regarding the production of crops from the year 2014 to 2017?

What are the aspects of agricultural development regarding farmers low budget criteria and how can governmental agencies handle this crisis?

What are the GDP targets regarding farmers infrastructure development at agricultural lands?

The state of Specialized Micro Finance Institutions in Bhutan

As we consider micro finance establishments in Bhutan, we understand that it is still in an incipient stage. Country credit in Bhutan was begun in 1980. It was ordered for Bank of Bhutan (BOB) to loan 44% of its portfolio in country credit, be that as it may, it loaned under 1% of its portfolio. The reasons were ranchers’ failure to meet the security and assurance prerequisite of the BOB and RICB (Royal Insurance Corporation of Bhutan). At that point, the provincial loaning program was depended to Food Corporation of Bhutan in 1980. Nourishment Corporation of Bhutan acquired cash at 14% enthusiasm from BOB and RICB and re-loaned the sum at 6% to 10% to agriculturists. This program kept going just two years. The program was then moved to Royal Monetary Authority (the national bank of Bhutan). As BOB and RICB were discovered one-sided towards general exchange, transport, and land, it was felt important to build up a different budgetary establishment to give advances to mechanical and farming related exercises. In this unique circumstance, with the marking of Royal Charter (RC) on January 31, 1988, Bhutan Development Finance Corporation Ltd. (BDFC) (which is right now known as Bhutan Development Bank Limited (BDBL)) was built up. At that point, the rustic credit program was given over to BDFC. From that point, forward BDFC (now, BDBL) has been executing Agricultural Credit in Bhutan.

Other casual methods for loaning to ranchers likewise exist in Bhutan as portrayed by Hussein (2019, for example, moneylenders, who exist inadequately in a few districts and charge an enthusiasm of 3%-5% and well to do families and people who additionally advance out to poor villagers now and again. Different banks incorporate devout foundations that loan at a higher rate of 15%-25%, and semi-formal loaning organizations, for example, the National Women Association of Bhutan (NWAB), which goes for giving gifted preparing and gathering loaning to ladies in country zones. The organization depends on the Grameen Bank model and advances are progressed with an enthusiasm of 14%.

In any case, regardless of consistent endeavors by the administration, rustic cr alter confronts real hindrances, as portrayed by Pathak (2010). Factors, for example, the scattered low populace, uneven territory, low foundation advancement, low advance recuperation rate, high hazard and high overhead cost have reared the effect on the improvement of micro finance establishments in country zones of Bhutan. In 2010, under 44% of ranchers approached credit from balance uncial establishments, (this was out of an expected 87,500 homestead families), and this figure was impressively lower for littler agriculturists at around 10%. The nonattendance of other committed micro finance foundations and the peak smaller scale fund body in Bhutan being BDBL alone has altogether controlled the extent of micro finance in the nation. From the customers’ point of view, few loaning establishments bringing about constrained access to advances, long and antagonistic obtaining techniques, contract pre requisites notwithstanding for little credits, high financing cost structure, and so forth., has postured huge hardships in getting advances.

On the off chance that we consider ventures made by money related establishments in Bhutan by segments, agribusiness comes in eighth, with add up to speculation by monetary divisions (as advances), which is a pitiful 1.39% of aggregate venture (adding up to Nu. 36,005.02 million) in the year 2010 (from the Statistical Yearbook k of Bhutan 2011, National Statistics Bureau , RGoB). Taking a gander at the pattern over a time of years, the rate of assets given to agribusiness regarding credits by budgetary organizations has really diminished from 1.92% of every 2016 to 1.39% out of 2010.

In fact, of the ten biggest parts which represented more than 99% of the credits, the best five were individual, Building and Construction, Manufacturing, Trade and business, Service and

Personal Loans for Agriculture

The above diagram obviously demonstrates the carelessness and lack of concern towards farming part loaning by monetary establishments. In the year 2010, an aggregate of Nu.499.45 million was put by money related foundations in the agribusiness part. In the event that we consider the expansion in interest in agribusiness area, there has scarcely been an increment of more than 105% contrasted with five years prior (somewhat finished twofold). In the examination, individual credits have expanded about five times and, vehicle advances (for overwhelming vehicles) have expanded more than six times (Statistical Yearbook of Bhutan 2011, RGoB).

Of the credits given to horticulture division in 2010, 99.10% originated from BDBL. Just a little rate of the advances was given by Bank of Bhutan (0.60%) and T-Bank (0.30%). The loaning rate in horticulture segment (for advances rendered by budgetary organizations) was static at 13% in the vicinity of 2018 and 2010 (for a reimbursement time of 10 years), though in the ‘other traveler vehicles’ part, financing costs really descended from 14% (for reimbursement in 5 years) in 2018 to 12% (for reimbursement in 7 years) in 2010 (Statistical Yearbook of Bhutan 2011, RGoB).

A current overview directed in Samtse has demonstrated that micro finance customers in Bhutan apparently obtained Nu.30, 000 to Nu.50, 000, and paid an enthusiasm of 5 to 10 percent to Bhutanese moneylenders or, 3 to 10 percent to Indian moneylenders. This is really a little sum, and shouldn’t require security by any stretch of the imagination. Such credits can be effectively given by specific micro finance organizations and can truly go far in helping the agriculturists in the midst of need.

While the improvements in the rural segment have made expansion openings, there are imperatives that can hamper the capacity of agriculturists; particularly that dominant part of Bhutanese ranchers are poor and peripheral agriculturists. The absence of sufficient framework, restricted access to data, credit, and different resources (land, water, and mechanical know-how), can seriously compel the extent of broadening activities.

These boundaries, data holes, and limit confinements display an open door, as well as a requirement for specialists’ concerned (Ministries, offices, contributors) to offer help and help to manufacture the limit with respect to expert poor broadening exercises.

Expansion activities require a multi-segment approach including numerous particular venture ranges. Approach and institutional condition, water system and seepage, science and innovation, and country framework are only a couple of illustrations. Every one of these speculations won’t originated from the general population part.

For long haul arranging, government needs to make the empowering conditions for the private segment to give sources of info and administrations to ranchers important for enhancement; (FDIs), be that as it may, the administration needs to contribute to enlarge the extent of research establishments to cover rising issues of broadening, enhance the scientific capacities of agriculturists to blend the expansion opportunity, and build up the productive learning and data frameworks.

Besides wage era, broadening will, in many cases, increment work for the country poor. For instance, von Braun evaluates that because of broadening to send out vegetable creation in Guatemala, work expanded by 45 percent on members’ homesteads. It is normal that the advantages of expanded business openings are significant as well as are circulated over a wide range of the economy and in this way are to a substantial degree “expert poor.”

Ali and Abedullah (2012) exhibited the potential for country work era emerging from enhancement out of oats to high-esteem products, for example, vegetables, by looking at the work force in the two frameworks. Considerable business openings are created in seed and seedling generation, accuracy arrives planning, and the water system, collecting, cleaning, evaluating, and bundling of high-esteem crops.

It was evaluated that a one-hectare move of grain to vegetables in one season creates over one year round all day business (that is, the contrast amongst oats and vegetables was more than 220 working days for each hectare). The off-cultivate work impact of comparative greatness was anticipated through the extension in the farming business exercises. Joshi and Gulati et al. (2012) likewise detailed comparative outcomes.

Because of developing customer interest for exceedingly bundled and prepared horticultural items, enhancement ordinarily includes the development far from customary wares (requiring negligible auxiliary preparing) toward higher esteem products (requiring critical preparing and dealing with). Moreover, the new creation frameworks are regularly more concentrated and produce interest for a more prominent amount and an assortment of homestead inputs.

Since high-esteem crops, contrasted with oats, are all the more emphatically interlinked with different divisions of the economy regarding giving their yields and accepting contributions from these segments, there is a more grounded multiplier impact of the underlying increment in pay. For instance, it was evaluated that a unit increment in beginning salary in oats has a multiplier impact of two, while comparable increment in vegetables will create a multiplier impact of three (Ali and Abedullah 2012).

With the move far from subsistence harvests to more beneficial money crops like vegetables, comes back to arrive, work, manure, and water are fundamentally higher. The level of change in cultivating pay in the long and medium term will rely on the idea of relative changes in wage and use and in addition the degree of home utilization.

Country family units in Bhutan procuring the greater part of their salary from the generation of exportable merchandise will encounter a net welfare increase paying little mind to their utilization crate, while the effect for those families that are net customers might be vague, contingent upon the impact on nearby nourishment costs. Regardless, broadening will bring about more prominent nourishment security at the family unit level.

Given the above situation, the Royal Government should play a dynamic part in instigating manageable development by empowering economical generation frameworks in accordance with the accessible assets of agriculturists and micro environments of soil and land, catching on the regular focal points Bhutan has over its neighbors like India and Bangladesh. To advance the star poor enhancement with high-esteem crops, speculation ought to be coordinated to diminish yield change by creating stress-tolerant innovations and safe cultivars of these harvests and to enhance Homestead to showcase linkages.

In addition, approach advancements ought to animate market components to grow little ranchers’ association with the end goal of defeating the economies of scale issue and enhancing their entrance to business sectors and data. Preparing on little scale horticultural business improvement can likewise empower smallholder ranchers and landless destitute individuals to change.

With suitable arrangements, some of these speculations may originate from the private area, while venture identified with the foundation of makers’ association to enhance their capacity in investigating expansion openings and meeting the exploration needs identified with these open doors should originate from the general population private division joint effort. Delgado (a researcher at Agricultural field) perceived that there are three prerequisites for strategy level consolation of expansion.

In the first place, enhancement methodologies need to target staple sustenance generation and showcasing issues to such an extent that approaches accommodating more prominent nourishment security are composed and executed. Increments in high-esteem creation are not prone to happen unless nourishment security dangers are impressively brought down, especially with regards to Bhutan where at present a high offer of assets is given to subsistence sustenance generation.

Second, the exchange costs related with the stream of assets and items amongst areas and districts should be diminished. This is so picked up from the creation of surplus can stream to ranges delivering non-excess, which thusly are required to help the generation of surpluses.

Third, there is a need to advance non-conventional fares as a wellspring of remote trade to abroad markets. For example, comparative fare things along the lines of mushrooms, Cordyceps, apples, and oranges should be additionally broadened. This can be accomplished by putting resources into investigating, expansion, preparing and data frameworks of high-esteem crops, natural creation, restorative and sweet-smelling plants, and by creating the quality foundation. It requires supported endeavors to beat institutional and infrastructural limitations.

A further essential part of the administration is guaranteeing that ranchers have the ability to benefit from the innovative and market openings display in the outer condition. This type of maker strengthening requires sound instruction and expansion frameworks at all levels, and in addition meditation when important to conquer any boundaries to the stream of the market and specialized data and learning.

Decentralization (DYTs, GYTs) has made an instrument to encourage the procedure yet additionally fortifying of such bodies as far as overhauling know-how, and mindfulness is considered essential. The significance of giving the agriculturists a choice of choices for their generation ought to be perceived inside the projects and subprojects of vocal arranging.

The up and coming national nourishment security arrangements archive need to address both the nationwide generation and the neighborhood accessibility of sustenance in ranges with low efficiency as well as zones more suited for the creation of tradable products, for instance.

Wellbeing and sanitation must be elevated to completely abuse the welfare impacts of commercialization and expansion, and strategy should concentrate on preparing and work versatility programs on the grounds that “all things considered, the minimum diversifiable gift is most likely uneducated work” (Quiroz and Valdés 2011, p. 297).

Furthermore, ultimately, proper exchange arrangement is basic, particularly given that the nation has started participation to joining the World Trade Organization (WTO), openings are progressively fixing to the abuse of developing markets in remote nations.

Bhutan-Export Strategy, 2010, UNCTAD/WTO.Bhutan Trade Statistics Up To 30th June 2012, Department of Revenue & Customs, Royal Government of Bhutan.

Delgado, C. (2012) “Agricultural diversification and export promotion in sub-Saharan Africa.” Food policy, volume 34, number 7, pages 243-279.

Delgado, C. and A. Siamwalla (2012). “Rural economy and farm income diversification in developing countries.” In; Proceedings of the 23rd international conference of agricultural economists, August 2014, Sacramento, California. Pages 129-198.

Druk Seed Corporation, (2012) Strategic Options, Ministry of Agriculture, Paro.

Export Oriented Vegetable Production Proposal, (date unknown) Ministry of Agriculture.

Forest Resource Development Section, “Non-Wood Forestry Products, A Report on Thimphu & Paro Dzongkhags”.

Identification Mission for Agricultural Production Project/IPM Phase II Draft Report November 2013.

Joshi, P.K., A. Gulati, P. S. Birthal and L. Tewari. (2012). “Agriculture Diversification in South Asia: Patterns, Determinants, and Policy Implications”. RGoB, MoA-NCAP-IFPRI Workshop on “Agricultural Diversification in South Asia”. Paro, Bhutan. November 21-23, 2012. (paper and slide presentation) Policy, Strategies and Plans, October 2011. Engineering Division, DOA (9th Five Year Plan 2012-2017),.

Quiroz, J., and A. Valdés. (2015). “Agricultural diversification and policy reform”. Food Policy. Volume 44, Number 9, Pages 267-295

Renewable Natural Resources statistics, 2010, Ministry of Agriculture.

Renewable Natural Resources statistics, 2015, Ministry of Agriculture.

Renewable Natural Resources Section, 2012-2017, Ninth Five Year Plan Document, Ministry of Agriculture.

Statistical Year Book of Bhujtan, (2014). National Statistical Bureau, Royal Government of Bhutan.

Tobgay, Sonam (2015). “Small Farmers and Food Systems in Bhutan”. A paper presented at the FAO Symposium on Agricultural Commercialization and the Small Farmer, Rome.von Braun, J. (2015). “Agricultural Commercialization: Impacts on Income and Nutrition and Implications for Policy”.

Want help to write your Essay or Assignments? Click here.