Want help to write your Essay or Assignments? Click here

Budgeting for a Start-up Company

Budget to Implement for a Start-up Company

Starting a company can be a daunting task if not well planned. Creating a budget is an essential task for a start-up company and it can help one understand where the business is going and if it is on the right track. The accountant helps in giving financial information that helps managers, tax authorities, investors and others in making decisions about resources allocation in the budget.

A budget should be realistic and accurate for a certain company depending on its goals (Banham, 2009).It helps explain how a company will utilize its resources to attain its goals. The main aim of this paper is to explain a budget to implement in a start-up company that will help it reach its financial forecast.

Although budgeting is indeed more work, it pays off with many benefits. Some of these benefits include price setting, capital and credit procurement, flexibility, and forecasting. A master budget involves linked budgets of production costs, sales, purchase, and income. In the management of a company, it serves as the controlling and planning tool. It has two components, the financial and operational budget.

A business plan is a guide to owners, investors, and managers as a business starts and through its growth in different stages. Apart from a start-up plan, there exist several forms of business plans, which include internal, strategic, feasibility, operations business, and expansion plan (Livingstone, 2013).

Budgeting for a Start-up Company

Want help to write your Essay or Assignments? Click here

A manufacturing company is a company that converts raw materials to finished goods. The consumer buys the finished goods directly or another manufacturing business uses them for making a different product. For the purpose of this paper, a bakery will be the manufacturing company. Value chain is a series of activities that add value to a company. The bakery company value adding activities are of two types, these include primary and support activities. The activities in the primary type include,

Inbound logistics, this will entail the receiving of raw materials.

Operations, this is the manufacturing stage which involves conversion of wheat into baked items.

Outbound logistics will help in the distribution of the baked goods to consumers.

Marketing and sales, this will involve identifying customer’s needs and generating sales for the company.

Services, this activity will provide after sales support services for the consumer.

The secondary activities will be in four categories, which include human resource management, business infrastructure, technological development, and supply chain management. Business infrastructure activity will involve organization of structure, culture, and control systems. Human resource management will involve employee’s recruitment and training. Technological development activity will entail having information technology to support the value chain and the company. Supply chain management will entail purchasing materials, equipments, and suppliers for the company (Hornyak, 2008).

Budgeting for a Start-up Company

Want help to write your Essay or Assignments? Click here

An operating budget is the analysis of asserts, expected costs, and predicated income over a specific period. This type of budget will be appropriate for the bakery company. The budget must account for factors such as material coast, production, labor cost, sales, manufacturing costs, and administrative expenses. The budget is manageable on a weekly, monthly, or yearly basis.

The operating budget also provides a way for a company to estimate its immediate future expenses and revenues. Several reviewing steps are necessary in ensuring the company attains its goals, these steps include, review of business goals against performance, review of budget variance, and access issues associated with budget overages (Livingstone, 2013).

The idea behind benchmarking is to make ensure that its services, products, and practices are the best against their competitors. Four benchmarking process will be utilized in the bakery company these includes,

Process benchmarking this demonstrates how top bakery companies accomplish specific task that earn them success. Interviews, site visits, and research are ways of obtaining information.

Performance metrics this involves use of qualitative measures as the reference for comparisons.

Strategic benchmarking this identifies winning strategies and lessons that have enabled top bakery companies to be successful.

Financial benchmarking involves a financial analysis of the bakery comparing it with top performers in order to assess the company’s competiveness.

Budgeting for a Start-up Company

Want help to write your Essay or Assignments? Click here

Benchmarking has several benefits, which includes, clarity of specific areas of opportunities, set performances expectations, and enable monitor and manage company’s performers (Hornyak, 2008).

Cost accounting involves collecting, analyzing, summarizing, and evaluating numerous alternatives to help managers take the most suitable course of action in the management of the company. The bakery will implement process costing as its type of costing systems. Process costing is a system that allocates direct and indirect cost for the manufacturing process. It assigns goods in large amounts.

The system is important since it will help the company keep track of the expenses in the production and distribution of goods. For example, the company may produce large number of bread but they may sell in small quantities, therefore it is necessary to allocate total product costs to units of product. One of the challenges that the company will face due to this system are costs errors.

Process costing does not allocate direct costs to individual goods leading to cost errors. This leads to increase in production cost thus increase in consumer product price. The company will implement the value chain analysis to overcome the problem that will help reduce the non-production cost thus creating the greatest possible value and price for consumers (Banham, 2009).

Budgeting for a Start-up Company

Want help to write your Essay or Assignments? Click here

For a start-up company to be successful it needs to draft a well-planned budget. This budget determines the success or failure of a company. By using this vital tool, one is able to track company’s expense, asserts and revenue required to keep the company growing. It may also help the company identify problems before they arise and be able to solve them. Therefore, a budget is like a roadmap for a company.

References

Banham, R. (2009). Better Budgets. Journal of Accountancy , 40-63.

Fearon, C. (2010). The Budgeting Nightmare. CMA Managment , 100-112.

Hornyak, S. (2008). Budgeting Made Easy. Management Accounting , 25-40.

Livingstone, J. L. (2013). The Portable MBA in Finance and Accounting. Accounting , 83-95.

Budgeting for a Start-up Company

Want help to write your Essay or Assignments? Click here

Want help to write your Essay or Assignments? Click here

Quantitative Financial Plan

Introduction

A budget is a quantitative financial plan for a specified period of time. The financial plan includes sales volumes, expenses, resource quantities, liabilities, assets and cash flows. The budget provides the details for strategic management (O’Hoyt, 2014). Budgets assist in financial planning of the actual business or production of certain products (Williams, Haka, Bettner & Carcello, 2008) Budgets also coordinate different organizational activities and also control resources, provide transparency and accountability (Bragg, 2010).

Budgets, financial plan are also used to forecast the requirement of future financial needs of the company. The financial performance of a company can also be analyzed by comparing the actual budget from the standard budgeted. The variance analysis provides the management with enough information to reorganize its operations and also to investigate any losses that may not have been anticipated (Bragg, 2010).

Cash budget on a monthly basis for six months ending June 30th 2016

Sharp 6 Months Cash Budget Ending June 2016

Details

Jan

Feb

Mar

Apr

May

June

Sales

247500

262500

277500

277500

360000

360000

Wages ( 6 employees)

7830

7830

7830

7830

7830

7830

Jones Salary (Director)

5600

5600

5600

5600

5600

5600

Purchases

256500

222300

199500

222300

256500

273600

Other Expenses

1060

5300

5300

5300

5300

4240

Loan Repayments

3250

3250

3250

7844

7844

7844

Total Expenses

274240

244280

221480

248874

283074

299114

Net Income

-26740

18220

56020

28626

76926

60886

Balance B/fwd

7844

-18896

-676

55344

83970

160896

balance C/Fwd

-18896

-676

55344

83970

160896

221782

The net income is a loss of 26,740 in January 2016 while the balance brought forward for the same period reduces the amount carried forward to a loss of 18896. The highest sales are expected in the months of May and June. The total purchases as a percentage of sales adds up to 80.2% of the total sales. The director’s salary is 2% of the total sales. Loan repayments total to 1.86% of the total sales.

The total expenses are estimated to 88% of the total sales (Garrison, Noreen & Brewer, 2009). That means that the Net income expected is just about 12%. The financial performance trends for the budget are shown on the table below. In February 2016 the total sales would grow by 6.06% whereas in March the same year the total sales would grow by 5.71%. There sales growth would be zero in the months of April and June.

But in May 2016 the sales would grow by 29.73%. The expected cost of purchases is also expected to in February and March by 13.33 and 10.26%. For the remaining months the cost of purchases would increase by 11.43%, 15.38% and 6.67% for the months of April, May and June (Aranya, 1990).

Want help to write your Essay or Assignments? Click here

Cash budget for six months ending June 30th 2016 with 15% sales reduction in final three months

When the total budget is adjusted downwards by 15% of the total sales for the last three months as forecasted below;

The sales would decrease from 277500 to 235875 in April while in May and June the sales would decrease from 360,000 for both May and June to 306000 for both months. These reductions would result in reduction of net income with approximately the same percentage.

The total net income for April would be a loss of 12,999 from the initial amount of 28626 before the 15% reduction. In May and June it would amount to 76926 and 60886 compared to the net amount after the 15% reduction which amounted to 22926 and 6886 (Garrison, Noreen & Brewer, 2009).

Sharp 6 Months Cash Budget Ending June 2016

Details

Jan

Feb

Mar

Apr

May

June

Sales

247500

262500

277500

235875

306000

306000

Wages ( 6 employees)

7830

7830

7830

7830

7830

7830

Jones Salary (Director)

5600

5600

5600

5600

5600

5600

Purchases

256500

222300

199500

222300

256500

273600

Other Expenses

1060

5300

5300

5300

5300

4240

Loan Repayments

3250

3250

3250

7844

7844

7844

Total Expenses

274240

244280

221480

248874

283074

299114

Net Balance

-26740

18220

56020

-12999

22926

6886

Balance B/fwd

7844

-18896

-676

55344

42345

65271

balance C/Fwd

-18896

-676

55344

42345

65271

72157

When the sales are reduced by 15%, the total sales in May and June would decrease from 360,000 to 306,000 for both months (Hermanson, Edwards, & Invacevich, 2011). The most notable trend is that the total amounts that would be carried forward would register a higher margin of growth when the sales are decreased by 15% (Anderson and Sedatole, 2013).

Want help to write your Essay or Assignments? Click here

Sales Reduced By 15%

Sharp 6 Months Cash Budget Ending June 2016 Trend Analysis

Details

Jan

Feb

Mar

Apr

May

June

Sales

6.06

5.71

-15.00

29.73

0.00

Wages ( 6 employees)

0.00

0.00

0.00

0.00

0.00

Jones Salary (Director)

0.00

0.00

0.00

0.00

0.00

Purchases

-13.33

-10.26

11.43

15.38

6.67

Other Expenses

400.00

0.00

0.00

0.00

-20.00

Loan Repayments

0.00

0.00

141.35

0.00

0.00

Total Expenses

-10.92

-9.33

12.37

13.74

5.67

Net Income

-168.14

207.46

-123.20

-276.37

-69.96

Balance B/fwd

-340.90

-96.42

-8286.98

-23.49

54.14

balance C/Fwd

-96.42

-8286.98

-23.49

54.14

10.55

The recommendation to the management is that the forecasted budget presents a profitable future for the company and should be implemented as all the purchases and all other expenses would have been paid off by the second month even when the sales are reduced by 15%. However, the cost of sales is very high and should be reduced (White, Sondhi and Fried, 1997). The net income margin of 12% is too small.

When the sales are reduced by 15%, the purchases would increase by 11.43% in April while in May and June purchases would also decrease by 15.38% and 6.67% respectively. Total expenses however would increase by 12.37% in April and 13.74% in May while in June total expenses amounted to 5.67%.

The net income would reduce by 12.2 percent in April while in May and June the Net income would reduce by 278.37% and 69.96% compared to the increase in initial Net Income of 168.73% and a reduction of 20.85% in May and June respectively. The increment of 10.55% after a reduction of 15% compares relatively to the initial increment of 37.84% on the total balance carried forward (White, Sondhi and Fried, 1997).

Sharp 6 Months Cash Budget Ending June 2016

Details

Jan

Feb

Mar

Apr

May

June

Totals

% of Sales

Sales

247500

262500

277500

277500

360000

360000

1785000

Wages ( 6 employees)

7830

7830

7830

7830

7830

7830

46980

2.63193277

Jones Salary (Director)

5600

5600

5600

5600

5600

5600

33600

1.88235294

Purchases

256500

222300

199500

222300

256500

273600

1430700

80.1512605

Other Expenses

1060

5300

5300

5300

5300

4240

26500

1.48459384

Loan Repayments

3250

3250

3250

7844

7844

7844

33282

1.86453782

Total Expenses

274240

244280

221480

248874

283074

299114

1571062

88.0146779

Net Balance

-26740

18220

56020

28626

76926

60886

213938

12

Balance B/fwd

7844

-18896

-676

55344

83970

160896

288482

balance C/Fwd

-18896

-676

55344

83970

160896

221782

502420

Want help to write your Essay or Assignments? Click here

Conclusions and recommendations

To conclude, the growth in total sales would continue to increase throughout the rest of the year as predicted by the trend hence the future of the business is very bright. The company should continue and implement the budget as planned. The total sales amounted to 2.6% of the budgeted sales while purchases were the highest expenses and it amounted to 80.2% of the total sales.

Loan repayments amounted to 1.9% of the sales. The company would remain profitable as long its operational costs don’t exceed the 80.2% range. The reduction in sales by 15% would result in a reduction of 69.96% in net income (Allaboutbudgets, 2015).

References

Anderson, SW & Sedatole, KL 2013. ‘Evidence on the cost hierarchy: The association between resource consumption and production activities’. Journal of Management Accounting Research (25): 119-141.

Aranya, N 1990. ‘Budget instrumentality, participation and organizational effectiveness’, Journal of Management Accounting Research (2): 67-77.

Garrison, R, Noreen, W & Brewer, P 2009. Managerial Accounting. McGraw-Hill Irwin New York.

Hermanson, RH, Edwards, JD & Invacevich, SD 2011. Accounting Principles: A Business Perspective. First Global Text Edition, Volume 2 Managerial Accounting, 37-73. McGraw Hill. Boston.

White, G, Sondhi, A. & Fried, D 1997. The Analysis and Use of financial statements, Wiley Press. New York. Williams, JR, Haka, SF, Bettner, MS. & Carcello, JV 2008. Financial & Managerial Accounting, McGraw-Hill Irwin. Boston

Want help to write your Essay or Assignments? Click here

Want help to write your Essay or Assignments? Click here

Balance sheet Financial Reporting

The balance sheet captures the current financial position of the NGO. Net assets should balance with the liabilities and equity since the each of the asset is funded by the resources contributed by members and other sponsors. The statement should provide a snapshot of the assets, liabilities, and net assets as the specified date. Gabel’s statement of financial position gives detailed information about the financial position of the company as indicated by the figures. It has the assets section, the liabilities section, and the equity section.

Each fixed asset should have its book value minus the depreciation to get the current net value. By giving the value of the asset in a different line with its total depreciation value makes the balance sheet untidy and crowded making it hard to analyze (Elizabeth, 2010). The net of the fixed asset is the one used to analyze the current financial position of the organization. It is therefore important to indicate the net of the fixed assets to avoid confusion. Deductions and accruals should just indicate the total amounts instead of individual amounts since the receipts will be attached to the statement to avoid congesting the statement.

Since the company is a non-profit, the balance sheet should only indicate the assets and the liabilities. The assets and liabilities are the values used to indicate the financial position of the organization and not the equity hence the net income and equity are not inclusive.

Also, it is important for the accountants to indicate the previous year’s balance sheet values for comparison purposes. The current values should be shown against the previous year’s or, at least, the past three years to make the analysis of the statement viable. When the values of two periods are shown, it makes it easy for analysts to make comparisons and understand the changes that may have taken place to get the current balance sheet values.

Want help to write your Essay or Assignments? Click here

Income Statement

The statement is used to give information regarding the operating activities of the organization from one date to another. It gives information pertaining the revenues and expenses during a particular time, and it’s useful to forecast future activities. For NGOs, activities are measured as received and used contributions. The statement is divided between temporary, restricted, unrestricted, and permanently restricted activities.

Recorded revenues should be classified into one of the four activities based on the donor’s intent. Expenses should be divided into the program, administrative, and fundraising expenses. Revenues are either in the form of activities, membership dues, program revenues, special event and investment income. By categorizing revenues and expenses in the different classification, it provides for better analysis as well as being in line with the global accounting standards.

Gabel’s statement does not give columns for the different activities under income and expenses. By generalizing the revenues and expenses and indicating their categories randomly makes it hard for analysis and is not in line with the required reporting standards. It is also important that the statement also records prior year values for comparison purposes. Categorizing each activity and expense into the section they fall helps stakeholders identify gaps in the company for improvement.

Want help to write your Essay or Assignments? Click here

Statement of cash flows

Statement of cash flow is used to record the cash inflows and cash outflows over a specified period. The statement is divided into three sections: cash flows from operating activities, cash flows from investing activities, and cash flows from financing activities (Ron, 2013). The total amount from the three sections gives an explanation of how the cash flow from the beginning of the period was converted to the balance at the end of the operating period.

Gabel’s statement should show the net cash for each of the sections and sum up the amounts resulting from same activity instead of detailing each activity. The statement is supposed to provide an overview of the cash flows to make it easy for reporting.

Accrual accounting

NGOs have a stringent requirement of using the accrual method of accounting as per the Generally Accepted Accounting Standards (Elizabeth, 2010). The accrual method records revenues when earned and expenses when they have been incurred. By using the accrual method, an organization can indicate its current financial position in a pronounced manner than the cash accounting method.

As an NGO, it is possible to get donors that offer to donate at a later period and when the amount is recorded, it gives the organization a stronger financial position. If Gabel uses the accrual methods, it can recognize pledges of donations and income when they have been made and record cash when it has been received making the income higher than if it used the cash accounting. Cash accounting only considers income when cash has been paid and expense when the amount has been disbursed making it hard to present the current financial position of the organization.

As long as a transaction is to take place and all the necessary conditions have been met then it should be recorded in the financial statements. With addition of statement of activities to the three financial statements, the company should apply accrual accounting to all its recordings not only to meet the required regulations but also to enable stakeholders have a correct view of the current financial position of the firm.

Want help to write your Essay or Assignments? Click here

Recommendations

1. Gabel’s Company should increase its campaigns to reach to more people hence increase its chances of donations. Though the company has net profit, it has a lot of activities it requires to attend to and perform using its wide assets base. Through fundraising campaigns, more donors will be attracted to pay and if they are followed up, they may end up increasing the contributions amount hence increasing the net realized income.

2. Another method the company can use is to increase member’s contributions and subscription fees as well as holding part of dividends to investment in rentals. The amount contributed by members can be added up at a small percentage with respect to individual member’s contribution and set of activity. If each member’s contributions is increased by a small margin, the total amount will subsequently increase helping to cover up for the administrative and other expenses to have a high income at the end of the period.

3. The company should also dispose of some of its unused assets before they lose their value. The amount generated can then be used to invest in some of its productive investment activities. There is a lot of available assets that may be disposed of to increase the net income. Some of the depreciating assets should be sold and a portion of the land rented out or even sold to raise extra income for the company to facilitate its daily operations.

Want help to write your Essay or Assignments? Click here

Venture Capital and Private Equity

Background

One major question that clicks into the mind is how the private equity and venture capital is different. Mere because both are used to refer firms that sell their investment in equity financing after they have invested in an organization. For the matter of facts, there exists a significant difference between these two; first, it is the way the firm performs their duties when involved in the two types of investment.

Secondly, the funds are used to purchase a different sizes and types of companies, and thus, claim a different percentage of equity in their invested companies, Cumming, (2013). In a technical way, Metrick, (2011), defines the term private equity as the money or cash invested in a company that becomes a private company through the investment. At the same time, these scholars state that sometimes, this term is used to refer companies that other firms through leveraged buyouts (LBOs). On the other hand, VC is an investment in business in the concept, start-up or during the early years of their establishment.

The paper will look into the Skylock Enterprise, which is a company that deals with clothing products. Frankly, speaking this is a fascinating company to be part of since established two years ago. Each and every day there a new opportunity present itself to build the great legacy we dream of. This company has grown into an integrated manufacturer of the highest quality clothes. This company operates one big plant located in the United States, seven outlets that provide retail services to our business.

In total, there are 543 employees for this company and walk home with over $100 million annual revenue, plus other health benefits (notably, the paper will work with US dollar unless otherwise stated). This company has a stellar reputation since its establishment in those two operational years. Its strongest suites being cotton clothes, women’s wear, men’s wear, as well as the children’s clothes.

Despite its good starting, this company is faced with a lot of challenges in the future. Skylock, manager Stanley White sees impending danger as there is a great competition from the large multi-national companies like Nike, Ralph Lauren among others. Great scholars like Ahlers, (2013), competition in most cases theoretically results in lowering the prices of the commodities, hence if this happens it can narrow the marginal revenue of the company.

Thus, this may limit the development and expansion of this great visional company. This makes the manager question whether this company will remain as innovative as it is, or does it need to adopt some changes. Thus, the major question remains, where Skylock Enterprise will focus its effort.

Due to the market condition in the United States, our company is a price taker, and we need to work on the set market price. In particular, we operate in a free market where no firm or entity has the ability to influence the prices in the market, Dix‐Carneiro, (2013). To succeed, we have to work with the price constraint and at the same time deliver the best quality goods. In fact, quality products always win the customer’s heart. This is in accordance with the factors that affect the demand for a commodity one being the quality (which affect the taste), the price among others Mankiw, (2014).

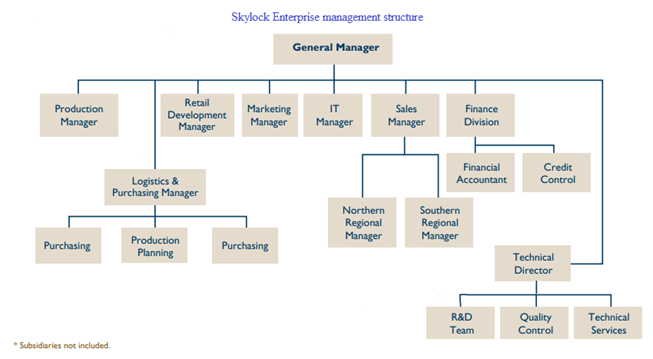

The Skylock company has excellent structure and one general manager who overlooks all the activities of the enterprise. Figure 1 is a management structure which portrays the general overview of the management team.

The primary focus of the firm in two years has been in the sales department since it plays an import role in advertising the company’s product. The core aim of this department is to increase the sale by two digit percent. Critical to note, in the two years of operation, the company revenue has risen by 5% and 8.6% consecutively. Thus, we are aiming at increasing this percentage to about 13%, this seems impossible, but through the proper financing of our sales, for appealing the commercial market is more oriented to the direct marketing than mass advertisement Danaher, (2011).

The statistics indicate that the firm used almost the same amount in direct marketing and advertisement. Hence, it will be ideal to adopt the direct marketing. Furthermore, the database used to target our marketing indicates that there has been an increase from 500 to 2500. This database includes suppliers and persons targeted specifically.

Skylock Enterprise also is also planning to produce newsletters and brochures that feature new designs and clothes in the market. This will be supplied free to opened outlets and any other targeted market, newsletters will also if there is, recent studies carried out by the firm. This will ensure that the customers are in the know what is going on with the company. Involving the company to the progress of an organization creates trustworthy and thus the customers feel more welcomed Mankiw, (2014).

Nevertheless, as compared to the main competitors to our company, we advertise less often. Taking into consideration that most of these firms have been in business for a long time. Thus, we need to advertise more often so that people can know about our existence. The aim is to raise the expenditure by 20% and target some of the new television series, which will quite improve company’s sales. The advertisement will majorly focus on all the brands in our store.

One of the greatest challenges that faces Skylock Enterprise is that it does not have many retail outlets as compared to its competitors. The location of the seven stores is in the main cities in the US. It is vital to operating our own retail shops since most of the larger firms (our competitors) control retailers. This has limited our sales as we solely depend on that seven retail for the entire revenue generation. The risk that the company faces the reputation risk, if it were to be damaged, the customers will become wary of doing business with us.

This will have not only an effect on the losing the customers, but also the revenue, and worst the sponsors and advertisers may turn their back on us. That is the reason we have a technical director that work with research and design team (R&D team) and the quality control department to ensure that all is well. The R&D department, more importantly, needs to be trained well, so as to keep the company with the trending fashions and also the market structure.

A second risk that this company may face is the financial risk. In particular, the cash that is flowing in and out of the organization, and the possibility of sudden financial loss. Our firm extends credit to some of the largest clients, hence, if they fail to pay on time or fails totally, then we are prone to incur a significant financial risk. To reduce the risk, the firm intends to operate at minimum credit services, and if it happens, it will be extended only to the few trustworthy customers, and it will only be a short-term credit. This is as suggested by the great economics scholars like Horcher, (2011).

Value Enhancement

As stated earlier, there are some of the strategies that the company is planning to undertake so as to improve the business performance, especially increasing sales volume. The firm first has prioritized the strategies and noted the objectives of each plan. First is the direct marketing strategy, which aims at increasing the sales, exploring the market and at the same time take the commodities to customers at their convenience places. Danaher, (2011) stipulates that direct marketing is convenient and also increases sales, especially when the products are unique and of high quality.

In fact, this is as a result of the impromptu purchase of the customers. The key measure that will be used to evaluate the success of this strategy is the use of consumption metrics. This is one of the many methods used to measure the content market success Parmenter, (2015). Importantly, they help in understanding the consumption behavior of customers to a particular piece of content. Thus, this will help Skylock to understand which design has high demand. The set strategy primary mandate is to increase sales by 10 percent.

The second strategy that Skylock will take to improve returns is increasing the number of retail outlets in different parts of US cities. This will be a way of ensuring that we expand the channels through which we reach our esteem customers. Furthermore, it is a method of increasing our market (through geographical coverage). This will increase the sales by about 50-77 percent.

The key performance indicator that will be employed to evaluate the success of this strategy is through data collection and analysis. As stipulated, the core purpose of data analysis is to understand their meaning, so as the firm can understand where the improvement opportunity lies Parmenter, (2015). Analysis will encompass all the sales made through all the Skylock’s retail outlets so as to determine whether the objectives have been fully met.

It is vital to note, before adopting any strategy, the firm will evaluate and decide the frequency at which they will collect relevant data on the achievement of the plan. At the start, the first step will be to assess the market effectiveness, which will be done weekly, and then can go to monthly to reduce the evaluation cost and so on. This is important since it also ensures that the marketing goals are set, KPIs are defined, and people to collect and analyze data are determined.

Want help to write your Essay or Assignments? Click here

Management Structure and Incentive Scheme

The incentive scheme in the firm will be (a must) transparent, for all the staff members understand all the mechanism involved in the calculation. Simply because, a well-designed scheme has a powerful and positive effect, increasing the productivity, quality, and importantly efficacy of an institution Brealey, (2012). Conversely, a poorly designed staff incentive scheme will have a detrimental effect on the overall company performance.

Thus, the main objectives of this scheme will be achieved, which is increasing performance level, change the attitude and/or change the behavior of the staffs. Key to note, the introduction of incentive program results in an increase in revenue as well as boost the company’s reputation (which is one of our risks).

Staff incentive is paramount for the development of an institution and at the same time exciting. Some of the most benefiting parties of this strategy are the shareholders (owners), clients, employees as well as the creditors Brealey, (2012). To start with the owners, this includes even the Venture Capital and Private Equity investors, since the firm’s performance increases drastically through these measures. This aligns with the objectives of the owner, that is, to improve the achievement to a certain degree, and also reducing the standard financial performance. In other words, reducing the financial risks.

In addition, incentives should be directed to the management team of the institution. This is because the success of this organization and its reputation entirely depend on the managers. In other words, they have been delegated the duties of ensuring the firm’s objectives are met. Sometimes, this separation of management and ownership can be problematic as owners may lack means to make the managers perform their best to achieve the firm’s goals.

Further, the managers give the employees some duties, and they are supposed to make a decision and take actions. Thus, it is vital to ensure that incentives are designed in a way that even employees execute their duties are the top management will want.

The incentive scheme will motivate the whole team to work on achieving the organization’s goal. This will, on the other hand, increase the revenue return which in turn increases the cash the stakeholders receive for their capital contribution. To sum all up, the best strategic plans that Skylock Enterprise can adopt for their success have been well illustrated. This will make them more competitive, build a high reputation, and more importantly, increase their revenue, of which it is the core principle of establishing a business.

References

Ahlers, R., Schwartz, K. and Guida, V.P., 2013. The myth of ‘healthy’competition in the water sector: the case of small scale water providers. Habitat international, 38, pp.175-182.

Brealey, R.A., Myers, S.C., Allen, F. and Mohanty, P., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Cumming, D.J. and Johan, S.A., 2013. Venture capital and private equity contracting: An international perspective. Academic Press.

Danaher, P.J. and Rossiter, J.R., 2011. Comparing perceptions of marketing communication channels. European Journal of Marketing, 45(1/2), pp.6-42.

Dix‐Carneiro, R., 2014. Trade liberalization and labor market dynamics. Econometrica, 82(3), pp.825-885.

Horcher, K.A., 2011. Essentials of financial risk management (Vol. 32). John Wiley & Sons.

Want help to write your Essay or Assignments? Click here

Principles of Financial Accounting

Major accounting concepts and conventions used in accountancy form the major guidelines and rules of the accountant’s life. Historical cost accounting convention is a technique in accounts that ensures valuation of an existing benefit for the balance sheet at the cost of the asset at its purchase.

Assets, revenue, and expenditures are recorded at the money’s worth that was historically paid to complete the transaction (Deegan 2013). All the items in the financial statements are recorded at what cost the company for an item and not the fair market value and not what the company could currently sell the item.

The major criticism of historical cost is that it considers the cost of acquisition despite this cost of an asset not recognizing the current market value. It only interests itself in the cost allocated and not in an asset’s value. It tells the acquisition value and decrease in succeeding years but ignores the likelihood of the present market worth of the asset being elevated or lower than its suggestion (Miles 2015).

Historical costs also exhibit an obvious fault during times of inflation. Its validity rests on an assumption that currencies for recording the transactions remain stable or stagnation of the purchasing power. During inflation, the price of an asset rises, however, the corporate finance model’s objective centers on creating value for shareholders.

Want help to write your Essay or Assignments? Click here

The main advantage of historical cost is that the accounts are straightforward in producing them. The original value of the asset is known and recorded thus based on an actual value and not an estimation of value. Historical costs do not also record gains to the company until full realization is realized thus, presenting the actual performance of a company. Historical cost accounts further are still utilized under many accounting systems such as the GAAP that requires the value of an asset recorded at its historical costs with an exception of marketable securities (DRURY 2013).

The alternative methods or bases introduced by IASB is the Capital Maintenance in Units of Constant Purchasing Power, that allows for the quantification of financial assets maintenance in ostensible monetary units or in units of purchasing control that can be constant regardless of deflation or inflation levels (Kaplan et al., 2015). The major advantage of this technique is that it allows the management to make a judgment when applying or developing an accounting policy when there is an absence of interpretation applying to a transaction.

The major disadvantage of this system is that it provides no applicable international standard for financial reporting with regards to the assessment of invariable but real value items that are non-monetary. These may include share capital that has been issued and capital reserved. It is also not chosen by accountants in non-hyperinflationary economies despite its automatic maintenance of the actual worth of non-monetary items with steady genuine value (Van Dooren et al., 2015).

Want help to write your Essay or Assignments? Click here

An analysis of the qualitative analysis indicates that historical cost accounts are easily understood because it is based on original costs. The values are relevant because it is a true representation. The values can however not be reliable on the verge of hard economic times.

However, comparability is possible depending on the underlying assumptions and the judgment of the management. Alternative bases by IASB are relevant because they represent the current economic conditions (DeVellis 2012). They are easy to understand and compare the figures hence, reliable as a tool for financial reporting.

Historical cost is the most appropriate basis for measurement in financial reporting. The underlying factor here is that it is free of any bias information and is follows the GAAP procedures. It is also simple and a more conventional method and helps in leading to absolute certainty by fitting perfectly with the statement of cash flow.

Kaplan, R. S., & Atkinson, A. A. (2015). Advanced management accounting. PHI Learning.

Van Dooren, W., Bouckaert, G., & Halligan, J. (2015). Performance management in the public sector. Routledge. DeVellis, R. F. (2012). Scale development: Theory and applications (Vol. 26). Sage publications

Want help to write your Essay or Assignments? Click here

Want help to write your Essay or Assignments? Click here

Madison Plc Funding Analysis

Introduction

Organizations are usually formed with an objective of gaining profit and attaining growth. This means that the management of an organization is always aimed at ensuring that operations are in the right order for such to happen. This calls for various processes to be initiated for the purpose of proper operation. Firstly, proper strategic planning has to be carried out.

Secondly, the finances of an organization have to be organized so that the reported results may be impressive. To understand better, company analysis is necessary since it gives a brighter picture of an organization’s financial status. This report will focus on Madison Plc for analysis. It will give a detailed explanation of the various funding sources that Madison Plc can have for its expansion plans.

Additionally, the advantages and disadvantages of each source of funding identified will be explained deeply. For better understanding, the report will also focus on the ways that Madison Plc can manage the sources of funding for better results. In the main part of this report, matters related to management of working capital will also be highlighted.

For better understanding of this company’s investment options, analysis of different options will be highlighted and implications outlined properly. Additionally, the report will show ratio analysis of two companies that it is aiming at acquiring; thus getting an opportunity to make a choice. In the conclusion part of this, a summary of the main point will be indicated for better understanding.

Want help to write your Essay or Assignments? Click here

Funding

For most organizations, getting adequate funding is one of the major challenges of being in business (Johnson, Scholes & Whittington 2007, p. 12). This is because resources are usually scarce, and money is part of scarce resources. Madison Plc has to seek more funding for the purpose of expanding its operations across the globe as planned. This means that the company has to look for the sources of more money. The different sources of funding that Madison Plc can utilize are explained below.

Debt financing

Debt financing refers to raising capital for a business through getting loans or credit facilities from lenders (Gupta 2011, p. 43). This means that an organization may go ahead and apply for financing in some of the known lenders. Interestingly, companies are known to rely on lenders as a means of accessing more capital for its operations (Kaplan & Norton 2004, p.98).

Therefore, Madison Plc can move ahead and approach some of the available lenders for funds to push forward its expansion agenda. This may be done through various arrangements; Madison Plc may get into an agreement with lenders regarding the percentage amount of gain to share. Secondly, the parent company and Madison Plc may agree on the payment period for any more financing granted.

Want help to write your Essay or Assignments? Click here

Advantages of debt financing

Debt financing is associated with various benefits. One of the advantages of using debt financing is that the risk associated with giving some ownership to new investors is reduced. With debt financing, an organization obtains money from lenders who do not need any part of the company. As a matter of fact, debt financing connects the lender and an organization through the periodic payments.

Secondly, it does not subject an organization to divided control as is the case with equity financing. This means that decision making organ of the organization keeps on functioning normally. The third benefit of debt financing is that an organization is able to have more money as retained earnings. It has been observed that despite the fact that the company pays interest on debt, the amount of money spared which would have gone to additional investors witnessed in equity financing.

Disadvantages of debt financing

One disadvantage of debt financing is that the company bears the burden of debt management. Having taken financing from loans, an organization has to ensure that the facility is properly management (Kaplan and Norton 2006, p.89). The burden of following up on the repayment records is tedious and a burden to an organization. Additionally, debt financing involves more cost for an organization. According to Arnold (2009, p.24), going for debt financing means that an organization has to pay interest to cover the cost of getting the credit facility.

Want help to write your Essay or Assignments? Click here

Equity financing

Equity refers to the shares of an organization. Therefore, Madison Plc can use equity as to fund its operations. Through equity, this company can invite interested investors to purchase some shares in the company. This will make the investors shareholders while the company benefits from the money paid for the shares.

Advantages of funding through equity

One advantage of equity financing is that it creates a possibility of meeting people who are beneficial to an organization. Having investors purchase the shares of a business may create the benefit of having knowledgeable people form part of new investors. The benefits may also come as a result of having new investors who have more resources to lend to the organization. Having more able people get in the ownership of a business is always very important.

This is because the new investors may extend more money for use in the operations of an organization. Additionally, the new shareholders may be able to give the organization beneficial business connections. According to Hill and Jones (2007, p.19), new owners of a business may bring about the much needed network in the business community.

The second benefit of equity financing as a source of capital is that there is no burden involved in management of credit facilities. It is worth noting that whenever an organization gets into debt, there is always need to have proper credit management, something which is not experienced with equity financing. The burden of extra cost incurred through payment of interest is not experienced with the use of equity financing.

Want help to write your Essay or Assignments? Click here

Disadvantages of equity financing

Equity financing is known to have various disadvantages to an organization. The first disadvantage is that the new investors will have to get part of the company’s profits. According to Neale and McElroy (2004, p.16), important to note that shareholders are usually motivated by the share of profit that they get from an investment. This means that the profit of an organization will end up being divided among the increased number of shareholders. The second disadvantage of going for equity financing is that the management of an organization becomes more divided.

Equity financing is known to divide the control in management of an organization (Debarrshi 2012, p. 98). With shared control of the business, decision making process becomes complicated. Finally, equity financing is disadvantageous in that unnecessary disagreements may arise. This becomes more complicated if some of the new shareholders are not team players.

Retained profits financing

Retained profit is the other source of capital that Madison Plc can have. With retained profit as a source of capital, an organization usually ploughs back some of the earned profit. This means that instead of the profit being allocated for other purposes such as payment of dividends, the company uses it to carry out capital operations.

Want help to write your Essay or Assignments? Click here

Advantages of funding through retained profit

One advantage of financing the operations of a business through retained earnings is that the level of debt in the organization does not increase. With retained earnings, the business does not incur any cost such as interest on loans as is the case in debt financing. This means that an organization does not reduce its net profit as a result of financing expenses.

The second benefit of financing through retained earnings is that an organization maintains its independence. This means that the management of an organization is not diluted as a result of new investors in the shares of an organization. This means that the decision making process in the organization does not become complicated and unnecessarily long. Additionally, conflicts in the organization do not increase as would be the case with equity financing.

Want help to write your Essay or Assignments? Click here

Disadvantages of funding through retained profit

One disadvantage of using retained earnings as a source of capital is that it takes a long time before a considerable amount of money is ploughed back. It is worth noting that retained earnings reduce the speed with which an organization can grow through more investments. It is usually a very slow source of revenue. Secondly, retained earnings as a source of capital reduce the liquidity of an organization.

Using retained earnings to expand or have more investments means that cash for the business is reduced. This risks crippling other business commitments that require cash. Additionally, the use of retained earnings as a source of financing denies an organization an opportunity to gain from new members of the organization as is the case in equity financing.

Efficient working capital management in improving cash flow

It is worth noting that proper management of the working capital of an organization is very important (Gray, Salter & Radebaugh 2011, p. 34). This is because it contributes in shaping the well being of an organization. Madison Plc can do away with some of the non-current asset. Additionally, for proper management of the working capital of Madison Plc, long-term debt financing can be sought.

Want help to write your Essay or Assignments? Click here

Break-even analysis as a tool for decision making

Break-even analysis is a tool used in determining the level of operation in which an organization will be able to just cover its costs. At the break-even point of an organization, there is no loss or profit made from operations in place (Keller & Price 2013, p.56). Break-even point is usually indicated through showing that the income generated equals the total cost involved. For Madison Plc, break even analysis can be helpful in deciding which software to produce. This can be done through looking at the cost that would be covered by the returns.

Break-even point in terms of money= (1.57 units) × ($5,500) = $8,635

Therefore, the breakeven point is at the point where the sales stand at $8,635.

Profit=Sales-Total cost

=Total cost=$7,515

=$8,635-7,515=1,120

Madison Platform:

Assuming that the fixed cost = $8,500

And variable cost = $1,847 per unit

The price per unit of output=$6200

P × Q = Vc × Q + Fc

6,200 *Q = 1847Q + 8,500

6200 Q = 1847 Q + 8,500

6200Q – 1847Q = 8,500

4,353Q = 8,500

Q = 8,500 / 4,353

Q = 1.95 units

The BEP in units= 1.95 units

Break-even point in terms of money= (1.95 units) × ($6,200)

= $12,090

Therefore, the breakeven point is at the point where the sales stand at $12,090.

Profit=$12,090-Total cost

Total cost=$10,347

=12,090-10,347=$1,743

Loss

From the break-even points of the two options, Madison Plc should invest in Madison Platform since profit at the break-even point is higher than that of Madison Super.

Other factors a firm may take into account when making investment decisions

Making of investment decisions are usually very sensitive for an organization. This is because they determine the future of an organization. Investment decisions should be done with care since any mistake may lead to poor performance of organization. The other factor that Madison Plc may take into consideration when making investment decisions is the payback period of each investment option.

The payback period of an investment refers to the duration that an investment will take before the initial capital used is recovered. Therefore, Madison Plc should go for investment options that have the shortest payback period. According to Boddy (2005, p.80), an investment that has a short payback period is the best for an organization. A short payback period of an investment means that in a short while, an organization will start enjoying profit without considering the capital employed.

Want help to write your Essay or Assignments? Click here

The other factor that Madison Plc should consider when making investment decisions is the accounting rate of return. According to Proctor (2012, p.21), rate of return refers to the amount an investment pays back to the organization with regard to the capital involved. It is important for Madison Plc to go for investments with the highest accounting rate of return.

Ratio analysis of Puteaux France and Melia Portfolio Research Spain for consideration by Madison Plc

Financial ratio analysis is a tool used in analyzing the performance of an organization. Financial ratios are usually useful in scrutinizing various aspects of a business. For the purpose of decision making regarding the company that Madison Plc should invest in, the profitability, liquidity and efficiency ratios of Puteaux digital France and Melia Portfolio Research Spain will be calculated.

Liquidity ratio

Liquidity ratio measures capability of an organization to handle short-term commitments through the use of its short-term assets (Hermanson& James 2012, p.16). Some of the liquidity ratios for two companies are as calculated below.

The current ratio

Current ratio = Current assets

Current liabilities

Puteaux digital France

Short-term assets

Liabilities (short-term)

Current Ratio

2011

3,879

2,184

1.78

2012

4,457

1,490

2.99

2013

8,330

1,693

4.92

Melia Portfolio Research SpainCurrent AssetsCurrent LiabilitiesCurrent Ratio 2011 3,879 9,834 0.39 2012 4,457 13,490 0.33 2013 8,330 17,687 0.47

From the current ratios calculated above, Puteaux is seen to have the best relationship of current assets with current liabilities. The current assets are seen to cover the existing assets in more than 1 time. Under this ratio, Madison Plc should go for Puteaux digital France. According to Collier, (2009, p. 17), current ratio should not be too high.

Quick ratio

Acid test ratio = Current Assets – Stock

Current Liabilities

Puteaux digital France

Current Assets – stock

Current liabilities

Quick Ratio

2011

3,879

2,184

1.78

2012

4,457

1,490

2.99

2013

8,330

1,693

4.92

Melia Portfolio Research Spain

Current Assets-stock

Current Liabilities

Quick Ratio

2011

3,879

9,834

0.39

2012

4,457

13,490

0.33

2013

8,330

17,687

0.47

From the quick ratios calculated above, Puteaux is seen to have the best relationship of current assets with current liabilities less stock as indicated by the quick ratio, which is more than 1. The current assets are seen to cover the current assets in more than 1 time without consideration of the inventory. Under this ratio, Madison Plc should invest inPuteaux digital France.

Profitability ratios

Net-profit margin

Net profit margin Net profit x 100

Sales

Puteaux digital France

Net Profit before Tax

Sales

%

2011

1,658

9,406

17.63

2012

2,197

10,812

20.32

2013

2,395

11,516

20.80

Melia Portfolio Research Spain

Net Profit

Sales

%

2011

-1,387

15,529

-8.93

2012

-1,595

17,849

-8.94

2013

-1,833

20,516

-8.93

Considering the net profit margin, Madison Plc should invest in Puteaux digital France. This is because it has a high net profit margin compared to Melia Portfolio Research Spain. A high net profit margin indicates that an organization has a higher growth capability than another one whose net profit margin is low.

Return on Capital Employed

This is a measure of the gain realized in comparison with the capital invested.

Return on capital employed=Operating profit x 100

Capital

Puteaux digital France

Net Profit before Tax

Capital

%

2011

1,658

7,873

21.06

2012

2,197

10,069

21.82

2013

2,395

12,464

19.22

Melia Portfolio Research Spain

Net Profit before Tax

Capital Employed

%

2011

-1,387

4,910

-28.25

2012

-1,595

3,315

-48.11

2013

-1,833

1,482

-123.68

The return on investment of the two companies shows that Puteaux has a better return. This means thatPuteaux has been able to realize more gain on the capital invested. Therefore, Madison Plc should invest inPuteaux digital France since it has a higher net profit margin than Melia Portfolio Research Spain.

Want help to write your Essay or Assignments? Click here

Efficiency ratios

Asset turnover ratio

Asset turnover ratio measures the extent to which an organization’s assets have been utilized.

The asset turnover ratio = Sales Revenue

Net Assets

Puteaux digital France

Sales

Net assets

Asset turnover ratio

2011

9,406

7,873

1.19

2012

10,812

10,069

1.07

2013

11,516

12,464

0.92

Melia Portfolio Research Spain

Sales

Net assets

Asset turnover ratio

2011

15,529

4,910

3.16

2012

17,849

3,315

5.38

2013

20,516

1,482

13.84

From the calculations above, Melia Portfolio Research Spain is seen to be having a higher asset turnover ratio. This means that Madison Plc should be interested in putting his money on Melia Portfolio Research Spain than Puteaux digital France.

Upon analysis of the several ratios for two companies, most ratios are in favor of Puteaux digital France. Therefore, Madison Plc should confidently go for Puteaux digital France as the best investment option.

Recommendations

It is always important for organizations to ensure that actions that are fundamental in performance improvement are done in the earliest time possible. Therefore, it is significant for the management of Madison Plc to guarantee that all what is required for the purpose of making the investment plans successful is done early enough. Firstly, the management of this company should ensure that the source of financing for new investment is identified as soon as possible.

With several sources of finances being in place, it is reasonable to go for the option that gives the organization optimal results. Additionally, the company should look for the option that upholds the independence of the company. With this in mind, Madison Plc should go for debt financing as the source of finance for its projects.

Working capital management is a very fundamental aspect in business. Madison Plc should ensure that there is proper management of working capital for the purpose of creating sustainability of the current position of the organization. It is important for the company to guarantee that the best ways of improving the working capital of the organization are employed. Disposal of some long term assets should be done on time to create better current health in the organization.

Want help to write your Essay or Assignments? Click here

Conclusion

From the ratio analysis, it is evident that the company has been able to have a good performance. This means that ratio analysis should be carried out regularly to ensure that the various aspects of Madison Plc are understood well. Madison Plc should also ensure that proper working capital management takes place. This is important since it safeguards that the company improves its current health. Madison Plc should certify that there is good choice of investments.

According to Angwin (2007, p.46), investment decisions should always be made in such a way that encourages good performance and optimal performance. To succeed in making good investment decisions, the organization should use the available investment analysis tools. With this done, it will be possible to make all decisions regarding investments.

In terms of financing, the company should ensure that it goes for debt financing. This is good for this company since it will guarantee that there is independence in management. Additionally, debt financing will increase the value of retained earnings for the company.

Want help to write your Essay or Assignments? Click here

Budget: Financial Plan

Introduction

A budget is a quantitative financial plan for a specified period of time. The financial plan includes sales volumes, expenses, resource quantities, liabilities, assets and cash flows. The budget provides the details for strategic management (O’Hoyt, 2014). Budgets assist in financial planning of the actual business or production of certain products (Williams, Haka, Bettner & Carcello, 2008) Budgets also coordinate different organizational activities and also control resources, provide transparency and accountability (Bragg, 2010).

Budgets are also used to forecast the requirement of future financial needs of the company. The financial performance of a company can also be analyzed by comparing the actual budget from the standard. The variance analysis provides the management with enough information to reorganize its operations and also to investigate any losses that may not have been anticipated (Bragg, 2010).

Cash budget on a monthly basis for six months ending June 30th 2016

Sharp 6 Months Cash Budget Ending June 2016

Details

Jan

Feb

Mar

Apr

May

June

Sales

247500

262500

277500

277500

360000

360000

Wages ( 6 employees)

7830

7830

7830

7830

7830

7830

Jones Salary (Director)

5600

5600

5600

5600

5600

5600

Purchases

256500

222300

199500

222300

256500

273600

Other Expenses

1060

5300

5300

5300

5300

4240

Loan Repayments

3250

3250

3250

7844

7844

7844

Total Expenses

274240

244280

221480

248874

283074

299114

Net Income

-26740

18220

56020

28626

76926

60886

Balance B/fwd

7844

-18896

-676

55344

83970

160896

balance C/Fwd

-18896

-676

55344

83970

160896

221782

The net income is a loss of 26,740 in January 2016 while the balance brought forward for the same period reduces the amount carried forward to a loss of 18896. The highest sales are expected in the months of May and June. The total purchases as a percentage of sales adds up to 80.2% of the total sales. The director’s salary is 2% of the total sales. Loan repayments total to 1.86% of the total sales.

The total expenses are estimated to 88% of the total sales (Garrison, Noreen & Brewer, 2009). That means that the Net income expected is just about 12%. The financial performance trends for the budget are shown on the table below. In February 2016 the total sales would grow by 6.06% whereas in March the same year the total sales would grow by 5.71%. There sales growth would be zero in the months of April and June.

But in May 2016 the sales would grow by 29.73%. The expected cost of purchases is also expected to in February and March by 13.33 and 10.26%. For the remaining months the cost of purchases would increase by 11.43%, 15.38% and 6.67% for the months of April, May and June (Aranya, 1990).

Want help to write your Essay or Assignments? Click here

Cash budget for six months ending June 30th 2016 with 15% sales reduction in final three months

When the total budget is adjusted downwards by 15% of the total sales for the last three months as forecasted below;

The sales would decrease from 277500 to 235875 in April while in May and June the sales would decrease from 360,000 for both May and June to 306000 for both months. These reductions would result in reduction of net income with approximately the same percentage.

The total net income for April would be a loss of 12,999 from the initial amount of 28626 before the 15% reduction. In May and June it would amount to 76926 and 60886 compared to the net amount after the 15% reduction which amounted to 22926 and 6886 (Garrison, Noreen & Brewer, 2009).

Sharp 6 Months Cash Budget Ending June 2016

Details

Jan

Feb

Mar

Apr

May

June

Sales

247500

262500

277500

235875

306000

306000

Wages ( 6 employees)

7830

7830

7830

7830

7830

7830

Jones Salary (Director)

5600

5600

5600

5600

5600

5600

Purchases

256500

222300

199500

222300

256500

273600

Other Expenses

1060

5300

5300

5300

5300

4240

Loan Repayments

3250

3250

3250

7844

7844

7844

Total Expenses

274240

244280

221480

248874

283074

299114

Net Balance

-26740

18220

56020

-12999

22926

6886

Balance B/fwd

7844

-18896

-676

55344

42345

65271

balance C/Fwd

-18896

-676

55344

42345

65271

72157

When the sales are reduced by 15%, the total sales in May and June would decrease from 360,000 to 306,000 for both months (Hermanson, Edwards, & Invacevich, 2011). The most notable trend is that the total amounts that would be carried forward would register a higher margin of growth when the sales are decreased by 15% (Anderson and Sedatole, 2013).

Want help to write your Essay or Assignments? Click here

Sales Reduced By 15%

Sharp 6 Months Cash Budget Ending June 2016 Trend Analysis

Details

Jan

Feb

Mar

Apr

May

June

Sales

6.06

5.71

-15.00

29.73

0.00

Wages ( 6 employees)

0.00

0.00

0.00

0.00

0.00

Jones Salary (Director)

0.00

0.00

0.00

0.00

0.00

Purchases

-13.33

-10.26

11.43

15.38

6.67

Other Expenses

400.00

0.00

0.00

0.00

-20.00

Loan Repayments

0.00

0.00

141.35

0.00

0.00

Total Expenses

-10.92

-9.33

12.37

13.74

5.67

Net Income

-168.14

207.46

-123.20

-276.37

-69.96

Balance B/fwd

-340.90

-96.42

-8286.98

-23.49

54.14

balance C/Fwd

-96.42

-8286.98

-23.49

54.14

10.55

The recommendation to the management is that the forecasted budget presents a profitable future for the company and should be implemented as all the purchases and all other expenses would have been paid off by the second month even when the sales are reduced by 15%. However, the cost of sales is very high and should be reduced (White, Sondhi and Fried, 1997). The net income margin of 12% is too small.

When the sales are reduced by 15%, the purchases would increase by 11.43% in April while in May and June purchases would also decrease by 15.38% and 6.67% respectively. Total expenses however would increase by 12.37% in April and 13.74% in May while in June total expenses amounted to 5.67%.

The net income would reduce by 12.2 percent in April while in May and June the Net income would reduce by 278.37% and 69.96% compared to the increase in initial Net Income of 168.73% and a reduction of 20.85% in May and June respectively. The increment of 10.55% after a reduction of 15% compares relatively to the initial increment of 37.84% on the total balance carried forward (White, Sondhi and Fried, 1997).

Sharp 6 Months Cash Budget Ending June 2016

Details

Jan

Feb

Mar

Apr

May

June

Totals

% of Sales

Sales

247500

262500

277500

277500

360000

360000

1785000

Wages ( 6 employees)

7830

7830

7830

7830

7830

7830

46980

2.63193277

Jones Salary (Director)

5600

5600

5600

5600

5600

5600

33600

1.88235294

Purchases

256500

222300

199500

222300

256500

273600

1430700

80.1512605

Other Expenses

1060

5300

5300

5300

5300

4240

26500

1.48459384

Loan Repayments

3250

3250

3250

7844

7844

7844

33282

1.86453782

Total Expenses

274240

244280

221480

248874

283074

299114

1571062

88.0146779

Net Balance

-26740

18220

56020

28626

76926

60886

213938

12

Balance B/fwd

7844

-18896

-676

55344

83970

160896

288482

balance C/Fwd

-18896

-676

55344

83970

160896

221782

502420

Want help to write your Essay or Assignments? Click here

Conclusions and recommendations

To conclude, the growth in total sales would continue to increase throughout the rest of the year as predicted by the trend hence the future of the business is very bright. The company should continue and implement the budget as planned. The total sales amounted to 2.6% of the budgeted sales while purchases were the highest expenses and it amounted to 80.2% of the total sales.

Loan repayments amounted to 1.9% of the sales. The company would remain profitable as long its operational costs don’t exceed the 80.2% range. The reduction in sales by 15% would result in a reduction of 69.96% in net income (Allaboutbudgets, 2015).

References

Anderson, SW & Sedatole, KL 2013. ‘Evidence on the cost hierarchy: The association between resource consumption and production activities’. Journal of Management Accounting Research (25): 119-141.

Aranya, N 1990. ‘Budget instrumentality, participation and organizational effectiveness’, Journal of Management Accounting Research (2): 67-77.

Garrison, R, Noreen, W & Brewer, P 2009. Managerial Accounting. McGraw-Hill Irwin New York.

Hermanson, RH, Edwards, JD & Invacevich, SD 2011. Accounting Principles: A Business Perspective. First Global Text Edition, Volume 2 Managerial Accounting, 37-73. McGraw Hill. Boston.

White, G, Sondhi, A. & Fried, D 1997. The Analysis and Use of financial statements, Wiley Press. New York. Williams, JR, Haka, SF, Bettner, MS. & Carcello, JV 2008. Financial & Managerial Accounting, McGraw-Hill Irwin. Boston

Want help to write your Essay or Assignments? Click here

Want help to write your Essay or Assignments? Click here

Retirement Plans

Introduction

During the past three decades the retirement plans have shifted from Direct Benefit (DB) to Defined Contribution (DC).The trend is seen in both public and private sectors. The DC plans transfer much of the decisions like the investment and savings from the employer to the employee. The DC plans have attracted the employees in terms of their flexibility and portability.

The mentioned benefits come with the responsibility to choose in a wise manner. The plans have also provided the economists to study the saving behaviors of the individuals. In developed countries like US the plans have expanded themselves to several other factors like health care and time-off arrangements. Due to their wide adoption they have been implemented in different countries including Latin American Nations, Germany, Sweden and Russia.

As the power of decision is given to the individual it is assumed that the employee will behave as an active economic agent acting to maximize its self-interest. According to this implicit assumption it is assumed that the individual can interpret and judge the information presented as options from employees and governments. The individual is able to evaluate and balance the choices offered to him and can reach an informed decision.

In the recent years it is seemed that the people when trying to maximize the profitability make decisions which have less outcomes as expected. According to the studies the individuals have the right intention but they lack in the abilities to make necessary changes in the behavior. The philosophy of the people making such decisions has developed the rapidly increasing fields of behavioral economics and finance (Utkus et.al, 2003).

b) Purpose

This research will focus on the question of behavior adopted by the individuals while making economic decisions and the reaction of the market towards these decisions. In the research it will be analyzed that how the workers make decisions to save, manage the retirement investments and how they address their assets in retirement. The choices of making decisions have some consequences which are planned to be evaluated in this research. The research questions are as follows:

Are the employees well placed and informed about the plans offered by the employers or the governments?

How the DC plans are implemented in the various countries?

How the employees made decisions regarding their retirement plans?

Literature Review

Defined Contribution (DC) Plans in Various Countries

Stakeholders in the employment sector have an obligation of ensuring that retired employees attain the capacity of enjoying lifelong financial security. However, the approach of how and when this can be achieved remains a wide subject of discussion. Different nations across the globe adopt different mechanisms of implementing their policies regarding saving for the future. Defined contribution (DC) is one of the most adopted approaches of enhancing the employee saving concept for future financial security.

Edwards and Webb (2015)defines Defined Contribution as a retirement plan sponsored by the employer, which puts into account several factors like employee salary history and period of services. Under this scheme, the company exercises entire control of the investment risk and management of portfolio. According to Edwards and Webb (2015), the success retirement scheme is dependent on the input of the plan, levels of saving, and performance level of investments provisions relative to particular benchmarks.

However, these metrics do not sufficiently address the plans potential in providing employees with adequate retirement income. Similarly, there are several challenges, which the responsible institutions of implementing retirement schemes face in the line of deciding the most suitable retirement plan to employ (Beshears 2012). As a result, different countries employee employ different schemes suitable for the needs of its employees.

The objective of this paper is a literature review addressing how different countries implement defined contribution policy. This study also presents a discussion on the relevance of the said retirement plans and contribution schemes and some of the areas, which needs to be addressed to meet the needs of the participants.

Want help to write your Essay or Assignments? Click here

Implementation of Defined Contribution plan